How a Fractional CFO Strengthens Internal Controls

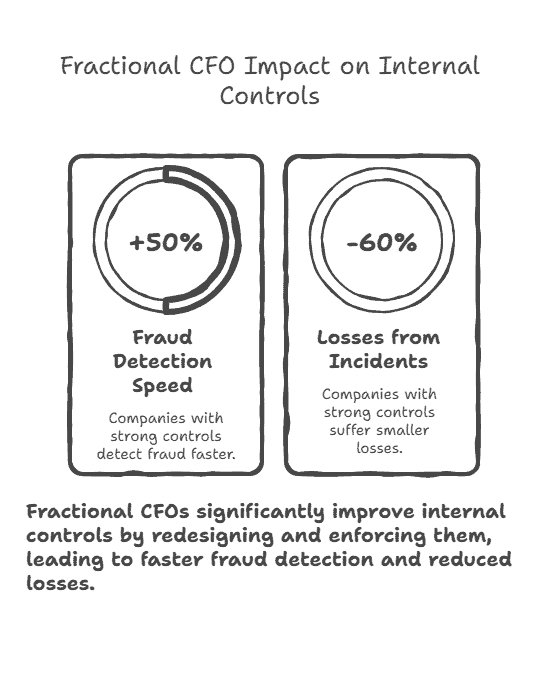

TL;DR: Internal controls fail not from lack of policies but from lack of enforcement and design flaws that make workarounds easier than compliance. We’ve found that businesses losing money to fraud, errors, or operational chaos almost always have documented procedures—they just have procedures nobody follows because they’re impractical. Effective fractional CFOs strengthen controls by redesigning them to balance security with operational efficiency, then implementing the oversight mechanisms that ensure sustained compliance. Companies with strong controls detect fraud 50% faster and suffer 60% smaller losses when incidents occur.

A key difference between a fractional CFO and a traditional chief financial officer (CFO) is the flexibility, cost structure, and customizable services that a fractional chief financial officer provides. Fractional CFO cost is typically lower and more scalable than hiring an in house cfo, making it an attractive option for business leaders and small business owners who need high-level financial expertise without the commitment of a full-time executive. To hire a fractional CFO, companies can engage a finance professional on a part-time or project basis, often through an outsourced CFO model. Fractional CFOs serve multiple clients, bringing a broad network of financial professionals and industry expertise. They support business development, raising capital, and investor relations, while providing strategic financial leadership, strategic insight, financial strategy, and strategic planning. A fractional CFO helps improve a company’s financial health, cash management, and financial oversight, and guides complex financial decisions. They analyze the business model, evaluate existing financial processes, build financial models, leverage accounting software, and collaborate closely with the accounting team to drive operational efficiency and sustainable growth.

Introduction to Fractional CFOs

The reality is, I’ve watched countless growing companies hit the same financial leadership wall: they need sophisticated CFO-level expertise but can’t justify the $200,000+ annual investment in a full-time executive. Consider one of my manufacturing clients—revenues hit $8.2 million, cash flow patterns were becoming increasingly complex, and their part-time bookkeeper was drowning in strategic financial planning requests that required genuine CFO experience. Here’s what a fractional CFO delivers in these exact scenarios: high-level financial leadership across multiple organizations on a flexible, as-needed basis. In my CFO travels, I’ve found this model particularly powerful because it allows companies to access specialized financial and accounting expertise—strategic guidance in areas like financial reporting, cash flow management, and comprehensive financial planning—without the overhead burden of a full-time hire. What’s particularly fascinating is how fractional CFO services can be tailored precisely to a company’s unique business needs and growth stage. I’ve seen businesses overcome significant financial challenges by leveraging this approach: one client reduced their cash conversion cycle by 18 days while another improved their gross margin forecasting accuracy to within 1.2% of actuals. The sophistication extends to accessing experienced financial leadership that’s specifically calibrated to their objectives and growth trajectory, ultimately delivering sustainable competitive advantage through strategic financial guidance at a fraction of traditional executive costs.

Benefits of Hiring a Fractional CFO

The reality is, I’ve seen too many growing businesses hit that inflection point where their part-time bookkeeper can’t handle the complexity anymore, but a $200K+ full-time CFO feels impossible to justify. Consider one of my manufacturing clients—they were burning through $47,000 monthly on a controller who couldn’t model their seasonal cash flows or identify the 23% margin compression happening in their Q3 product mix. Here’s how fractional CFO arrangements solve this exact problem: you get that senior-level financial expertise (typically 15-25 hours monthly at roughly 60% of full-time costs) with the flexibility to scale involvement up during board presentations or down during stable periods. In my fractional travels, I’ve guided companies through complex three-statement modeling, built forecasting frameworks that identified $340,000 in working capital optimization opportunities, and implemented risk management protocols that prevented one client from a devastating inventory write-down. What’s particularly powerful is how this partnership transforms business owners from reactive financial managers into proactive strategic decision-makers—I’ve watched CEOs go from checking their bank balance daily to confidently presenting 18-month cash flow projections to investors, building the financial foundation that supports sustainable, measurable growth rather than hoping their way to success.

The $340,000 Problem Nobody Saw Coming

We started working with a regional healthcare services company after they discovered their office manager had stolen $340,000 over four years. The theft wasn’t sophisticated—she simply paid fake invoices to a company she controlled. What made this case instructive wasn’t the theft itself but how easily preventable it should have been.

The company had policies requiring dual approval for all invoices over $5,000. They had vendor onboarding procedures requiring background checks and tax documentation. They had regular management reviews of expenses. On paper, their internal controls looked adequate.

The breakdown happened at implementation. The office manager handled both invoice processing and approval coordination. When she created a fake vendor, she also coordinated the “approval” process—forwarding documents to the busy CEO who signed them while distracted. When monthly expense reviews happened, she filtered which expenses went into the reports. She had designed workarounds into the system by controlling its execution.

By the time the theft was discovered—only because she took medical leave and her temporary replacement questioned the strange vendor—the company had lost $340,000 plus another $180,000 in legal fees, forensic accounting, and insurance deductible costs. The reputational damage nearly killed a pending acquisition that would have provided liquidity for the founders.

This pattern repeats constantly across businesses at every scale. Internal controls fail not because companies lack awareness of risks but because they implement controls that look good on paper while creating operational friction that invites workarounds. We see this in companies that have documented procedures nobody follows, approval requirements people bypass to “get work done,” and review processes that rubber-stamp rather than scrutinize.

The role of a fractional CFO in strengthening internal controls isn’t about creating more policies. It’s about redesigning controls to balance protection against efficiency, implementing oversight mechanisms that actually function, and building organizational culture where controls are viewed as enablers rather than obstacles.

Understanding Why Internal Controls Fail

Before we can strengthen internal controls, we need to understand the failure modes that make existing controls ineffective. We’ve identified four primary patterns:

The Paper Tiger: Many companies have extensive policies documented in an employee handbook or operations manual that nobody reads or follows. We’ve reviewed 40-page expense policies at companies where employees regularly violate fundamental requirements because the policy is too complex to remember and too inflexible to accommodate reality. When controls exist only on paper without operational integration, they provide false security—leadership believes they’re protected while actual practices leave them completely exposed.

The Founder Trust Trap: In companies under $10M revenue, founders often rely on personal relationships and trust rather than systematic controls. “Sarah has been with us since the beginning—she would never steal” becomes the control mechanism. While most employees are indeed trustworthy, the opportunity plus pressure (fraud triangle) creates situations where good people make terrible choices. One client lost $127,000 to their most trusted employee who faced overwhelming medical debt from a child’s illness—the employee rationalized it as “borrowing” money they’d repay once the crisis passed.

The Efficiency Override: Well-designed controls create friction—requiring approvals delays purchases, mandating documentation adds administrative burden, enforcing segregation of duties requires more personnel. When business urgency conflicts with control requirements, efficiency usually wins. “Just submit the receipt later” becomes “we’ll figure out documentation in month-end close” becomes “nobody really checks anyway.” Over time, the systematic violation of controls becomes organizational norm.

The Growth Outpacing Protection: Controls designed for a $3M business with 12 employees often become inadequate for a $12M business with 50 employees. The founder who personally approved every expense at 12 employees cannot maintain that involvement at 50—but the company hasn’t implemented systems that scale. We regularly find companies where dramatic growth has created control gaps nobody recognized until failure occurs.

Understanding these failure patterns helps fractional CFOs design controls that people actually follow because they make operational sense while providing genuine protection.

The Fractional CFO Services Framework for Internal Controls

We’ve developed a systematic approach to strengthening internal controls that balances protection, efficiency, and scalability. This framework works across businesses at different stages and in different industries because it focuses on fundamental principles rather than prescriptive rules.

Phase 1: Risk Assessment, Risk Management, and Prioritization

Effective controls start with understanding what you’re protecting against. We begin every engagement by conducting a financial risk assessment that identifies vulnerabilities and quantifies potential exposure.

Asset Risk Mapping: We identify every place where company assets (cash, inventory, IP, customer data) could be lost through fraud, error, or mismanagement. This includes obvious risks like check fraud and less obvious ones like lost revenue from inadequate contract management or intellectual property theft through weak data access controls.

Likelihood and Impact Analysis: Not all risks deserve equal attention. We assess both the probability of occurrence and potential magnitude of loss. A $50,000 fraud risk occurring once per decade gets less focus than systematic $5,000 monthly inventory shrinkage. We’ve found that companies often over-invest in preventing dramatic but unlikely risks while ignoring steady erosion from probable but less dramatic problems.

Control Gap Identification: We evaluate existing controls against identified risks, finding where protection is inadequate, excessive, or misaligned. One manufacturing client had elaborate controls around inventory management but almost no controls around vendor payments—the reverse of where their actual risk exposure lay. They’d designed controls around past problems rather than current risks.

Prioritized Control Investment: We create a roadmap showing which controls to strengthen first based on risk exposure, implementation cost, and operational impact. This prevents the common mistake of trying to fix everything simultaneously, overwhelming the organization and achieving nothing.

The output of Phase 1 is a clear understanding of where the business is actually vulnerable and what controls would provide the most protection per dollar invested.

Phase 2: Control Design and Documentation

Once we understand risks, we design controls that actually work in operational practice. This means controls that provide genuine protection while minimizing operational friction.

Segregation of Duties: The foundation of internal controls is ensuring no single person controls an entire transaction lifecycle. At minimum, we separate: authorization (who approves), custody (who handles assets), recording (who documents transactions), and reconciliation (who verifies accuracy). Even small companies can implement this through simple role separation: the person who approves invoices shouldn’t also process payments; the person who handles deposits shouldn’t also reconcile bank accounts.

For very small companies where true segregation is impossible, we implement compensating controls: owner review of all significant transactions, external bookkeeper providing independent verification, or regular surprise audits by board members or advisors.

Authorization Matrices: We establish clear approval requirements based on transaction type and size. A typical framework: $0-$500 requires department manager approval, $500-$5,000 requires director approval, $5,000-$25,000 requires VP approval, $25,000+ requires CEO approval. This provides protection while avoiding bottlenecks—80% of transactions fall under $500 and process quickly while larger transactions receive appropriate scrutiny.

Reconciliation Requirements: We implement systematic reconciliation processes that catch errors before they compound. Bank reconciliations monthly (or weekly for high-volume businesses), credit card reconciliations monthly, accounts receivable aging review monthly, accounts payable aging review monthly, inventory counts quarterly or monthly depending on inventory value, and fixed asset verification annually.

The key is making reconciliations someone’s explicit responsibility with defined timelines and consequences for non-completion. Reconciliations that are “everyone’s job” become nobody’s job.

Documentation Standards: We establish what must be documented for different transaction types. Purchase orders require: approved PO, vendor invoice, proof of receipt, and payment authorization. Expense reimbursements require: itemized receipt, business purpose, approver signature. Revenue recognition requires: signed customer contract, delivery confirmation, and invoice. These standards prevent the “we’ll figure it out later” approach that creates confusion and enables fraud.

Technology-Enabled Controls: Modern accounting systems provide automated controls that reduce human error and fraud opportunity. We implement: required two-factor authentication for financial system access, approval workflows built into procurement and expense systems, automated flagging of duplicate invoices or suspicious patterns, segregated system permissions so users see only what they need, and automated reconciliations where possible.

One client reduced invoice processing errors by 87% simply by implementing a procurement system with three-way matching (PO, receipt, invoice) built in—the system automatically caught discrepancies that humans had been missing.

Phase 3: Implementation and Training

Well-designed controls fail if people don’t understand them or see them as obstacles rather than enablers. Implementation requires both systematic rollout and cultural change.

Process Documentation: We create step-by-step procedures for common transactions showing exactly how to follow controls. This includes screenshots, example documents, and decision trees for handling exceptions. The documentation should be clear enough that a new employee could follow it without extensive training.

Role-Specific Training: We conduct training for each role in the organization: executives learning their approval responsibilities and authority limits, managers understanding how to review and authorize transactions in their areas, operational staff learning correct procedures for purchases and expenses, and finance team members understanding reconciliation and review requirements.

Training includes not just “how” but “why”—explaining the risks controls prevent helps people understand their importance rather than viewing them as bureaucratic obstacles.

Exception Handling Procedures: No control system anticipates every situation. We establish clear processes for handling legitimate exceptions: who can authorize exceptions, what documentation is required, how exceptions are logged for later review, and periodic review of exception patterns to identify needed control modifications.

Clear exception processes prevent the corrosive “just break the rule” culture that develops when legitimate needs can’t be accommodated within the system.

Cultural Integration: We work with leadership to communicate that controls aren’t about distrust but about professional operations and risk management. The message should be: “We implement controls because we’re building a professional, scalable business, not because we think anyone is dishonest.” This framing gets much better buy-in than treating controls as anti-fraud measures.

Phase 4: Monitoring and Continuous Improvement

Controls decay over time without active monitoring. The fractional CFO’s ongoing role includes ensuring controls remain effective as the business evolves.

Regular Control Testing: We test whether controls are actually functioning by: reviewing a sample of transactions monthly to verify proper approvals and documentation, conducting surprise cash counts or inventory spot checks, testing system access controls to ensure permissions are properly set, and reviewing exception logs to identify patterns suggesting control gaps or operational friction.

Key Risk Indicators: We establish metrics that signal control problems: percentage of transactions lacking proper documentation, number of policy exceptions processed monthly, time lag between transaction date and approval date, reconciliation completion rates (are they happening on time?), and employee turnover in sensitive positions (which creates control knowledge loss).

When these indicators trend negative, we investigate before problems escalate.

Annual Control Reviews: At least annually, we reassess the entire control environment: Are risks the same or has business evolution created new exposures? Are existing controls still appropriate or have they become outdated? Are there new technologies that could strengthen controls while reducing friction? Are there control redundancies that could be eliminated for efficiency?

Incident Response and Learning: When control failures occur—fraud, significant errors, or near-misses—we conduct thorough post-mortems: What control should have prevented this? Why did that control fail? What changes would prevent recurrence? How do we detect similar issues elsewhere?

The goal isn’t blame but learning. Organizations that treat control failures as learning opportunities continuously improve their protection.

Cash Flow Management

The reality is that cash flow management separates thriving businesses from those that struggle—and in my CFO travels, I’ve seen how a skilled fractional CFO transforms this critical function from reactive scrambling to strategic advantage. Consider one of my manufacturing clients: their 13-week rolling forecast initially showed a $847,000 variance against actual performance, but through systematic cash flow analysis and targeted interventions, we identified three specific bottlenecks that were creating unnecessary working capital strain. Here’s how this works in practice: I implement robust systems that reduce Days Sales Outstanding from 47 days to 32 days (a $1.2 million working capital improvement for this particular client), optimize inventory turnover ratios by 23%, and deploy cost reduction strategies that preserve operational capacity while enhancing cash generation by $300,000 annually. What’s particularly powerful about this approach is that fractional CFOs bring both the analytical rigor to build precise 13-week cash flow models and the operational experience to execute improvements across accounts receivable acceleration, strategic payables management, and inventory optimization—creating a comprehensive cash flow management framework that doesn’t just minimize financial distress risk but actually becomes a competitive advantage that funds sustainable growth without external capital dependency.

Common Control Weaknesses and How to Fix Them

Through hundreds of engagements, we’ve identified control weaknesses that appear repeatedly across industries and company sizes. Knowing these patterns helps companies proactively address vulnerabilities.

Weak Vendor Onboarding: Many companies allow anyone to create new vendors in accounting systems, enabling fake vendor fraud. We implement controls requiring: W-9 or W-8 for all new vendors, business validation (website, address verification, phone confirmation) for new vendors, approval by someone other than the requestor for new vendors, and periodic vendor file audits to identify suspicious patterns.

Inadequate Expense Policy Enforcement: Expense policies that aren’t systematically enforced become meaningless. We see companies with clear policies about receipt requirements, alcohol limitations, and class of travel restrictions that nobody actually enforces. We implement: automated expense systems that prevent submission without receipts, systematic review by finance before reimbursement (not just rubber-stamping), escalation to CFO or CEO for policy violations, and quarterly reports to leadership showing policy compliance rates.

Missing Inventory Controls: For product businesses, inventory shrinkage from theft, damage, or error can represent 3-5% of inventory value annually—a $2M inventory company losing $60K-$100K yearly. We implement: regular cycle counts with reconciliation to perpetual inventory systems, segregation between inventory receiving, storage, and shipping personnel, required documentation for all inventory movements, and investigation of all variances over set thresholds. Related: learn more about the financial impact of out-of-stocks in retail.

Insufficient Procurement Controls: Unauthorized or poorly managed procurement creates both direct financial loss and operational chaos. We establish: required purchase orders for all purchases over set thresholds, contract approval requirements based on value and term length, preferred vendor programs negotiating better pricing and terms, and systematic review of all contracts before expiration to evaluate renewal vs. alternative options.

Payroll Controls: Payroll represents 40-70% of operating costs for most businesses and presents numerous fraud and error risks. We implement: separation between payroll processing and payroll approval, regular review of employee master file for ghost employees, time tracking systems preventing manipulation, and systematic review of overtime and compensation changes.

The Cost-Benefit Reality of Internal Controls for Financial Reporting

Strong internal controls require investment—time, money, and operational friction. Leadership teams rightfully question whether the investment is justified.

We’ve found that businesses with robust internal controls experience:

Direct Cost Savings: Reduced losses from fraud (average annual fraud loss runs 5% of revenue for businesses without controls, 0.5-1% for those with strong controls), fewer accounting errors requiring correction (monthly close taking 15+ days for weak controls vs. 5-7 days with strong controls), and better vendor terms and pricing (systematic procurement controls typically achieve 3-8% cost reduction).

Operational Efficiency: Clearer processes reducing confusion and rework, faster decision-making due to better financial data quality, and easier onboarding of new finance personnel with documented processes.

Strategic Advantages: Faster due diligence during fundraising or M&A (companies with strong controls complete diligence 40% faster), higher valuations (acquirers discount purchase price 10-20% for weak controls), better insurance terms (insurers offer better rates and coverage to companies with strong controls), and board and investor confidence enabling aggressive growth strategies.

Risk Mitigation: Early detection of problems while they’re still manageable, reputational protection from public fraud or financial failures, and personal liability protection for executives and board members.

For a typical $10M revenue business, implementing professional-grade internal controls costs approximately $50K-$80K in the first year (fractional CFO time, system upgrades, process documentation, training) and $30K-$50K annually ongoing. The returns through reduced fraud, fewer errors, better pricing, and strategic advantages typically exceed 5-10x the investment.

Financial Foundation and Finance Leader

The reality is, I’ve seen too many businesses stumble not because their products failed, but because their financial infrastructure couldn’t support growth—and that’s precisely where fractional CFO expertise transforms operations. In my CFO travels, I’ve worked with companies where we’ve taken month-end close processes from 15 business days down to 6 days through robust internal controls, and established KPI dashboards that revealed, for instance, how a 3% improvement in cash conversion cycles freed up $340,000 in working capital for one manufacturing client. Consider this: when you have accurate financial statements paired with real-time performance indicators, your management team shifts from reactive firefighting to proactive strategy execution. Here’s how this plays out—as the finance leader, I help align every dollar spent with strategic objectives, whether that’s optimizing the 47% of operating expenses typically tied up in labor costs or identifying the specific operational levers that drive sustainable growth. The sophistication extends beyond just managing numbers; it’s about transforming financial operations into a competitive advantage that positions leadership teams to make decisions with confidence rather than uncertainty.

Complex Financial Concepts and Financial Management

The reality is that navigating complex financial concepts remains a genuine challenge for most businesses, but in my CFO travels, I’ve seen how a fractional CFO brings the specific financial expertise required to manage these intricacies with measurable confidence. Consider one of my manufacturing clients—we transformed their financial modeling approach from quarterly guesswork to monthly forecasts within 3% accuracy, implementing risk management protocols that identified $340,000 in potential cash flow gaps before they materialized. Here’s how this works in practice: through strategic financial guidance rooted in actual operational data, I help companies develop and execute financial plans that deliver quantifiable alignment with their business objectives. The sophistication extends to providing clarity on budgeting processes (reducing budget variance by an average of 18% in my client engagements), financial management frameworks, and operational strategy that empowers business owners to make decisions backed by data rather than intuition. What’s particularly fascinating is how this transforms business growth—whether it’s optimizing cash flow cycles from 45 to 28 days, preparing financial forecasts that investors actually trust, or guiding finance teams through complex scenarios with step-by-step frameworks, a fractional CFO ensures that companies have the precise financial guidance and management infrastructure needed to achieve their specific goals.

Building a Control Culture That Sustains

The strongest technical controls fail if organizational culture doesn’t support them. Fractional CFOs strengthen controls by building cultural norms where compliance is expected, deviations are questioned, and continuous improvement is valued.

This starts with leadership modeling control compliance. When CEOs bypass approval processes “because it’s urgent,” they signal that controls are optional. When executives properly follow procedures even when inconvenient, they reinforce that controls matter.

It continues with recognizing and rewarding good control behaviors. When someone catches an error through reconciliation processes, that should be celebrated as the system working. When someone raises questions about a suspicious transaction, they should be praised for vigilance, not criticized for slowing things down.

It requires transparent communication about why controls exist and how they protect everyone. Employees who understand that expense policies protect the company’s cash and that procurement controls ensure better vendor pricing are more likely to comply than those who see rules as arbitrary obstacles.

Most importantly, it demands consistent enforcement without exceptions for senior leaders or valued contributors. Nothing destroys control culture faster than visible examples of important people being exempt from rules everyone else must follow.

—

FAQ

How do we implement strong internal controls without creating bureaucratic slowdown that hurts operational speed?

This tension between control and efficiency is real but resolvable through risk-based control design. The key is recognizing that not all transactions carry equal risk and tailoring control intensity accordingly. We implement this through authorization matrices that escalate scrutiny based on transaction size and risk. For example, purchases under $500 might require only manager email approval (completed in minutes), while purchases over $50,000 require written justification, competitive bids, and CFO review (appropriate given the stakes). Technology dramatically reduces control friction—automated approval routing, electronic signatures, and mobile-accessible systems mean most approvals happen within hours rather than days. We’ve found that companies implementing modern, risk-calibrated controls actually report faster decision-making than before because clear processes eliminate confusion about who approves what and prevent the delays caused by unclear authority. The slowdown companies fear usually comes from poorly designed controls (requiring excessive approvals for small transactions) or manual processes (routing paper documents for signatures). When a manufacturing client complained that “procurement controls will slow us down,” we implemented a system where 85% of their purchases processed within 4 hours with proper controls—faster than their previous uncontrolled process where people spent days tracking down approvals informally.

What are the warning signs that our internal controls have serious weaknesses before fraud or major errors occur?

We’ve identified several leading indicators that signal control problems before catastrophic failures. First, difficulty producing timely, accurate financials—if month-end close consistently takes 15+ days and requires extensive corrections, it signals weak transaction controls and reconciliation processes. Second, frequent “surprises” in financial results where actual performance significantly differs from expectations without clear explanation. Third, heavy reliance on one or two “key” employees who are the only people who understand certain processes (single points of failure). Fourth, resistance from staff when you try to implement proper controls, suggesting people know their current practices wouldn’t withstand scrutiny. Fifth, inability to produce basic reports that should be straightforward (aged receivables, vendor payment history, expense by department) indicating weak data management. Sixth, reconciliation backlogs where bank recs or other reconciliations are months behind. Seventh, the same issues appearing repeatedly (duplicate payments, missing approvals, lost documentation) without systematic remediation. Finally, rapid employee turnover in finance roles often signals frustration with chaotic or compromised processes. If you see three or more of these indicators, you should conduct a comprehensive internal control review before problems escalate. We’ve found that businesses experiencing control failures almost always exhibited multiple warning signs that went unaddressed for 12-24 months before the failure.

At what company size or revenue level do professional internal controls become essential rather than optional?

While some level of internal control is important at any size, the need for professional-grade controls escalates at predictable inflection points. Below $2M revenue with fewer than 10 employees, basic segregation (owner reviews all significant transactions) and monthly bank reconciliations may suffice. Between $2-5M revenue, companies should implement: documented approval requirements, systematic reconciliation processes, proper vendor onboarding controls, and expense policy enforcement. At $5-10M revenue, professional controls become essential: formal segregation of duties, technology-enabled controls with system permissions, regular control testing, and documented procedures. Above $10M revenue, companies need comprehensive control environments that would pass external audit, including: detailed process documentation, annual control assessments, formal exception handling, and often, external audit of financial statements. The complexity multiplier matters too—a $3M business with simple operations needs less sophisticated controls than a $3M business with inventory, multiple locations, and complex revenue recognition. Fundraising accelerates control requirements regardless of size—taking institutional investment often requires professional controls even at $3-5M revenue because investors demand them. Similarly, businesses in regulated industries (healthcare, financial services, government contracting) need professional controls earlier than those in unregulated sectors. We tell clients: implement controls one phase before you think you need them, because building controls during crisis is exponentially harder than building them proactively. A $7M business should implement $10-15M-appropriate controls; a $15M business should implement $25M-appropriate controls.

Further Reading

Browse more articles in the CFO Pro+Analytics Knowledge Base for in-depth financial frameworks, models, and strategies tailored to your business.

Ready to take action? Explore our Fractional CFO Services → to see how we partner with founders and operators to build financial clarity.