The Fractional CFO Framework for Headcount Planning

Most companies treat headcount as an expense to minimize rather than an investment to optimize. Businesses with sophisticated headcount planning grow faster than peers while maintaining better unit economics, not through hiring more people but through hiring the right people at the right time with clear ROI frameworks. Effective headcount planning is not about saying no to hiring. It is about building analytical frameworks that enable confident yes decisions backed by specific financial models showing when each hire pays for itself and contributes to profitability.

Why Headcount Planning Goes Wrong: The $450,000 Mistake

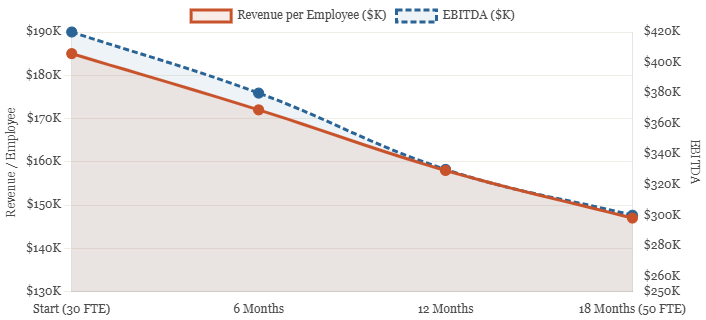

Consider a fast-growing marketing agency that had just hit its headcount target of 50 employees. The CEO was celebrating. The company had scaled from 30 to 50 people in 18 months, successfully delivering on its growth plan. When the financials were analyzed, a troubling pattern emerged.

Revenue per employee had declined from $185,000 to $147,000. Gross margin had compressed from 42% to 34%. Despite growing revenue 35%, EBITDA had actually decreased by $120,000. The company was working harder, serving more clients, and making less money.

The problem was not that they had hired bad people. The team was talented and hardworking. The problem was that they had hired without clear frameworks linking headcount to financial performance. They added an account manager because it felt like account management was stretched. They hired two designers because the design seemed overwhelmed. They brought on a business development director because enterprise sales felt like the next logical step.

Each individual hire made intuitive sense. Collectively, they destroyed value. The account manager covered only 3 clients instead of the 6 required for the role to be profitable. The designers specialized in work that the company could not sell enough of. The BD director focused on enterprise deals with 9-month sales cycles, while the company needed 45-day cash flow cycles to sustain operations.

When a proper headcount model was built with financial frameworks, the analysis showed they needed 8 fewer total employees but 4 different roles than those hired. The company spent 12 months realigning, including painful terminations. The total cost of misaligned hiring: approximately $450,000 in excess labor costs, over $200,000 in lost opportunity, and $85,000 in severance payments.

This pattern is not unique to this company. It repeats constantly across industries and growth stages. Companies hire based on intuition, workload perception, or org chart aesthetics rather than financial frameworks showing which roles generate returns and when. They celebrate headcount growth without analyzing productivity per employee or contribution to profitability.

Revenue Per Employee vs. Headcount Growth — Agency Case Study

What happened when hiring outpaced financial modeling — 30 to 50 employees over 18 months

The Three Questions That Drive Every Headcount Decision

Effective headcount planning begins with three analytical questions that must be answered before any hiring decision proceeds.

The first question is what financial return the role generates. Every role should have a clear articulation of how it contributes to the company’s financial performance. This does not mean every role must be directly revenue-generating, but every role should connect to measurable financial outcomes. Revenue-generating roles such as sales reps, account managers, and customer success positions should have clear productivity models. A sales rep should generate a defined amount of new ARR within a defined number of months. Cost-reduction roles in operations, procurement, and efficiency should quantify savings explicitly. Enabling roles such as support functions in finance, HR, and IT do not generate revenue directly but remove constraints that limit revenue-generating capacity.

The second question is when the role becomes profitable. Understanding time-to-profitability prevents cash flow crises and informs the timing of hiring decisions. The analysis requires modeling the fully-loaded cost of each role, not just the base salary. The fully-loaded cost calculation for a $75,000 base salary account manager runs as follows: add $15,000 in benefits, $5,000 for equipment and tools, $22,500 for training and onboarding at 25% of direct comp, and $15,750 for overhead allocation. Year-one fully-loaded cost: $133,250. If the role does not generate $133,250 or more in contribution margin, it is value-destroying regardless of how busy the team feels.

The third question is what happens if the company does not hire. Model three alternatives before approving any headcount request: redistribution to current employees, automation through technology, or simply delaying the hire by six months. Understanding the true cost of delay separates critical hires from convenient ones.

Fully-Loaded Cost Calculation — $75,000 Base Salary Role

- Base Salary: $75,000 — starting point only; never the number used for financial modeling

- Benefits (20% of base): $15,000 — health, dental, 401k, payroll tax, workers comp

- Equipment and Tools: $5,000 — laptop, software licenses, subscriptions allocated to the role

- Training and Onboarding (25% of direct comp): $22,500 — manager time, external training, productivity loss during ramp period

- Overhead Allocation (17.5% of direct comp): $15,750 — office space, IT systems, HR, and finance support services

- Year-One Fully-Loaded Cost: $133,250 — the actual financial bar the role must clear to create value

Building the Annual Headcount Budget Model

Once individual hire frameworks exist, the comprehensive annual headcount model connects hiring decisions to strategic objectives and financial targets. The headcount model begins with revenue and profitability targets and works backward to required organizational capacity. If a company targets $15 million in revenue from a $12 million base with 28% EBITDA margin, the calculation flows as follows: revenue increase required is $3 million; target EBITDA is $4.2 million; total operating expense budget is $10.8 million. If current headcount costs run $7.2 million, representing 60% of operating expenses, there is $3.6 million available for new hires while maintaining the same operating expense ratio.

Revenue per employee targets provide a second constraint. For a professional services business, revenue-generating roles should achieve $200,000 to $250,000 in revenue per FTE. Support roles should enable 4 to 6 times their cost in revenue capacity. Leadership roles should enable 10 to 15 times their cost in organizational capacity. If current revenue per employee is $155,000 and the target is $175,000, the company needs to either grow revenue faster than headcount, shift the hiring mix toward revenue-generating roles, or improve existing team productivity before adding capacity.

| Hire Type | Financial Return | Strategic Importance | Risk Mitigation | Overall Score |

| Senior Engineer | High — removes delivery constraint | Critical for product roadmap | Key-person risk exists | 9.0 / 10 |

| Operations Manager | High — 6-month payback, 2× ROI | Enables delivery scale | Removes a single point of failure | 8.5 / 10 |

| HR Manager | Medium — removes exec time cost | Enables scaling past 25 FTE | Medium — retention risk | 7.1 / 10 |

| Enterprise Sales Rep | High if ICP validated | Opens a new segment | Low — existing segment works | 6.8 / 10 |

| Additional Sales Rep | Medium — 14-month payback | Accelerates revenue growth | Low — team of 4 already | 6.2 / 10 |

| Marketing Analyst | Medium — attribution unclear | Supports demand gen | Low | 5.4 / 10 |

Scenario Planning and Headcount by Growth Stage

Three scenarios must be built into every annual headcount model so that when reality unfolds, the response is pre-planned rather than reactive. The optimistic scenario defines exactly which additional hires proceed and when if revenue exceeds targets by 20% or more. The expected scenario becomes the working model with hiring triggers tied to revenue milestones rather than calendar dates. The conservative scenario pre-defines which roles proceed and which defer when revenue falls 15% short of targets. When the business is tracking toward the conservative case, the team executes the conservative plan rather than freezing in place or making reactive cuts.

The approach to headcount planning also evolves as companies scale. At $2M to $5M revenue, every hire materially impacts burn rate and runway. Headcount planning focuses on clear ROI models with 12-month payback targets and heavy use of contractors before committing to full-time employees. At $5M to $15M revenue, the focus shifts to systematic capacity expansion while maintaining efficiency. At $15M to $50M, scaling through this range requires building a professional organization with leadership hiring that enables scaling beyond founder capacity. At $50M and above, headcount planning focuses on improving productivity and leverage, with aggressive revenue-per-employee targeting and systematic identification of low-value roles.

| Revenue Stage | Primary Focus | Hire Type Preference | Key Risk to Avoid |

| $2M–$5M | Burn rate and runway impact | Versatile generalists; heavy contractor use | Wrong FT hire = 6–12 months runway lost |

| $5M–$15M | Systematic capacity expansion | Departmental models; early specialist roles | Hiring for future company, not current size |

| $15M–$50M | Professional organization building | Leadership + clear accountability structures | Org structure mimicking larger companies pre-revenue |

| $50M+ | Productivity and leverage | Technology and outsourcing over headcount | Headcount inertia in low-value functions |

Common Headcount Planning Mistakes and How to Avoid Them

- The Utilization Fallacy: High utilization does not automatically justify hiring — first ask if low-value work can be eliminated or processes improved; adding 20% headcount often reveals 10% better processes would have sufficed

- The Org Chart Trap: Hiring to fill structural boxes rather than deliver financial returns creates overhead that does not generate value and slows decision-making

- Reactive Hiring Cycle: Hiring only when pain becomes acute creates feast-or-famine staffing; proactive planning hires in advance based on revenue triggers, not crisis response

- The Sunk Cost Trap: Retaining underperforming hires too long because of training investment; identify underperformance within 90 days and make a definitive decision within 180 days

- Misaligned Hire Timing: Approving the right hire at the wrong time relative to revenue milestones absorbs fully-loaded costs during zero production — hire timing must match the productivity ramp model

Building a Headcount Planning Culture

The most sophisticated headcount models fail if organizational culture does not support analytical hiring decisions. Culture change requires consistent norms that make intuitive hiring socially unacceptable and financial justification the standard expectation. Hiring requests should include a financial justification showing expected ROI and time-to-profitability before they are reviewed. Managers who bring requests without financial modeling should be sent back to build the model, not accommodated through intuitive approval. This norm, applied consistently, changes how managers think about headcount before they bring requests to leadership.

The conversation in leadership reviews should shift from do we need this person to does this hire deliver the returns required, given capital constraints and strategic priorities. When the question is framed financially, political advocacy for specific hires has less influence. The decision rests on which hire scores highest across the prioritization framework, not on whose champion is most persuasive in the room. Celebrating productivity improvements and revenue per employee growth as organizational achievements reinforces the culture shift. When the company communicates that growing revenue 25% with only 10% headcount growth is a win rather than evidence of underinvestment in staff, the organization learns to value efficiency over headcount scale.

FAQ

How do we accurately model productivity ramps for roles we’ve never hired before?

Modeling productivity ramps for new-to-company roles requires combining industry benchmarks, reasonable assumptions, and rapid learning. We use several approaches. First, industry data provides baseline expectations—if you’re hiring your first sales rep, sales productivity ramps are well-documented across industries and typically range from 6-9 months to full productivity. Second, interview candidates about their historical ramps in previous roles and factor in your company’s likely learning curve based on product complexity and market maturity. Third, examine analogous roles you have hired—if your account managers take 4 months to ramp, your first customer success manager will likely take 3-5 months given similar client interaction patterns. Fourth, build conservative first assumptions and commit to rapid model updates—plan for 9-month ramp but track actual productivity monthly, updating assumptions as you gather data. Most importantly, recognize that your first hire in a new role type is partially an experiment. One client hired their first enterprise sales rep with conservative 12-month productivity ramp modeled. Actual ramp was 8 months due to strong enablement and prior enterprise experience. When they hired the second enterprise rep, they had real data enabling better modeling. The key is being explicit about uncertainty (“we’re assuming 9-month ramp with 30% confidence”) and monitoring to replace assumptions with data quickly. This beats pretending you have precision when you don’t and enables faster learning.

What do we do when headcount models show we can’t afford the team we think we need?

This tension surfaces frequently—strategic plans require capabilities the financial model can’t support. Several approaches resolve this. First, challenge whether you truly need what you think you need. Can fractional or contract resources provide capabilities without FTE commitment? Can you achieve 80% of impact with 50% of investment through different role design? Second, phase hiring to match cash flow and revenue development. Rather than hiring 5 sales reps at once, hire 2, validate productivity and payback, then add 3 more in 6 months when cash flow supports it. Third, examine whether productivity improvements in existing team could reduce hiring needs—many companies discover that upgrading tools, improving processes, or providing better training enables current team to handle more capacity than new hires. Fourth, revisit strategic priorities—if financial constraints prevent hiring required team, perhaps the strategy needs adjustment rather than forcing financially unsustainable hiring. One SaaS client’s strategic plan required 8 new hires at $680,000 annual cost, but their cash position and revenue trajectory couldn’t support it. We restructured to 3 critical hires immediately, 2 contractors filling gaps, and 3 future hires contingent on hitting revenue milestones. This kept strategy viable while matching financial reality. Finally, if analysis shows you can’t afford needed team, that’s critical information for capital raising decisions. Many companies realize mid-analysis “we need to raise capital to fund this growth plan” rather than discovering cash crisis 6 months into hiring spree.

How do we balance headcount planning models with the reality that great people don’t wait for perfect timing?

This is perhaps the most common tension in headcount planning—you find an exceptional candidate, but they’re available now while your model says hire in Q3. We navigate this through several principles. First, truly exceptional people justify accelerating timelines if financial model permits any flexibility. A 10x performer hired 4 months early typically outperforms a 7x performer hired exactly on schedule. Second, create “opportunistic hire” budget in annual planning—setting aside 10-15% of hiring budget for unexpected great candidates enables saying yes without destroying the plan. Third, distinguish between “great person” and “great person for us right now”—many impressive candidates aren’t worth disrupting financial models if they’re not perfectly aligned with current needs. Fourth, maintain talent pipelines so when hiring timing arrives, you have 3-4 great candidates ready rather than starting sourcing from scratch. This reduces the “candidate timing doesn’t match our timing” problem. Fifth, use trial projects or consulting arrangements to engage great people before FTE commitment—if you find an amazing product marketer but your model says wait 5 months, bring them on for a 3-month project. If they’re truly great, convert to FTE. If not, you’ve validated before committing. The key is being honest about trade-offs. Hiring an exceptional sales rep 3 months early might cost $30,000 in accelerated cash burn but could generate $200,000 in incremental revenue if they’re productive quickly. That’s worth it. Hiring a good-but-not-exceptional operations person 6 months early costs $55,000 in accelerated burn with unclear benefits. That’s typically not worth it. Use financial framework to make rational trade-off decisions rather than emotional “we should hire great people whenever we find them” rationalization.

Conclusion: What is the strategic importance of headcount planning?

In conclusion, headcount planning is not just a one-time, tactical activity but a continuous, strategic exercise that integrates financial models, KPIs, and workforce data. Treating headcount planning as a strategic exercise ensures alignment with business goals, supports data-driven decision making, and drives operational efficiency. Conclusion headcount planning highlights its critical role in workforce management and organizational success, making it essential for companies aiming to scale effectively and remain agile in a dynamic business environment.