Month-End Close Optimization with a Fractional CFO

Most companies treat month-end close as a necessary administrative burden, consuming 15 to 25 days each month before financials are ready for analysis. An optimized close process delivers accurate financials in 5 to 7 business days while improving data quality and reducing accounting team stress. The benefit is not just faster reporting. It is faster decision-making, earlier problem detection, and the transformation of finance from a backward-looking reporting function into a forward-looking strategic partner. Companies with efficient close processes make business decisions 40% faster because they have timely, reliable financial data.

What Is a Fractional CFO and Why Does Month-End Close Matter?

Most growing companies hit a familiar inflection point somewhere between $5M and $15M in annual revenue. Their part-time bookkeeper can no longer handle strategic financial planning, but a full-time CFO at $200,000 or more per year feels financially out of reach. That is where a fractional CFO becomes genuinely transformational.

A fractional CFO is a senior financial executive who provides strategic financial leadership on a part-time or contract basis. This includes cash flow modeling, financial forecasting, investor-ready reporting, and operational finance. Unlike a full-time hire, the fractional model delivers the same high-level expertise at roughly 25 to 40% of the cost, with no equity packages, benefits overhead, or long-term salary obligations. Fractional CFO firms connect multiple companies with experienced financial leaders who deliver tailored solutions, making this model especially well-suited for startups and mid-market companies that need C-suite financial thinking without the full-time price tag.

Working with a $12M manufacturing client who reduced their monthly close from 22 working days to 8 days within 90 days illustrates the broader impact clearly. Reporting cycles accelerated, but more importantly, the business uncovered working capital inefficiencies that had been completely invisible under the old process. That is the real value of combining close optimization with experienced fractional CFO oversight.

The 22-Day Problem: A Real-World Example

Two years ago, I began working with a professional services firm generating $8M in annual revenue. They had a full-time controller and two accounting staff. The team was skilled and hardworking. The problem was timing.

January financials closed on February 25th. February financials closed on March 28th. March financials closed on April 22nd. Business leaders were making decisions in late April based on January’s financial data, information that was 90 or more days old by the time it informed strategy.

The consequences were concrete and costly. The company did not discover they had exceeded their Q1 sales compensation budget by $47,000 until late April, after commissions had already been paid and reversals would have created serious personnel issues. They did not realize that project margins on their largest client had compressed from 42% to 28% until March financials closed in late April, after they had already signed an expansion contract at similarly thin margins.

Most damaging was the opportunity cost. Leadership delayed hiring decisions, held off on market expansion investments, and deferred strategic initiatives because they did not trust their current financial position. The CEO later said: “I knew we were profitable, but I didn’t know if we were $200K profitable or $800K profitable. That uncertainty paralyzed decision-making for months.”

After rebuilding their close process, close time dropped to 7 business days while accuracy improved, and team stress reduced significantly.

Why Month-End Close Takes So Long: Five Root Causes

Before optimizing the month-end close, it is important to understand exactly where time is being lost. Across dozens of close optimization engagements, delays almost always fall into five categories.

Data Gathering and Consolidation: Many companies operate with multiple disconnected systems, an accounting platform for financials, a CRM for sales, an HRIS for payroll, spreadsheets for commissions, and a separate expense tool for reimbursements. Closing the month requires extracting data from every one of these systems and manually reconciling the inevitable inconsistencies that emerge. Accounting teams typically spend four to six days on this step alone.

Reconciliation Requirements: A proper close requires reconciling numerous accounts to ensure accuracy. Companies with weak reconciliation discipline spend five to eight days completing these reconciliations because they have allowed unreconciled items to roll forward across multiple months. Finding a $3,200 discrepancy from three months ago requires forensic accounting, not simple matching.

Accrual and Adjustment Requirements: GAAP requires matching expenses to the periods when they are incurred, not when they are paid. This means accruing expenses for services received but not yet invoiced, recognizing prepaid expenses ratably, calculating and recording depreciation and amortization, adjusting for unearned revenue and unbilled receivables, and recording payroll accruals when pay periods do not align with month-end. Companies without systematic accrual processes spend three to five days identifying what needs to be accrued.

Review and Approval Processes: After the initial close, financials require review at multiple levels, including the accounting manager, controller, CFO, and final CEO approval before statements are finalized. In organizations with weak close processes, reviews consistently reveal significant errors that require rework. Financial statements go through three or four revision cycles before approval, consuming four to six additional days.

Financial Reporting and Analysis: Companies still relying on manual Excel manipulation spend two to four days reformatting data, creating custom analyses, and building presentations. By the time those reports are complete, the financials are already 20 or more days old.

The Six-Element Framework for Close Optimization

Through dozens of close optimization projects, a systematic framework has emerged that consistently reduces close from 15 to 25 days down to 5 to 7 business days over a three-to-six-month implementation period.

Element 1: System Integration and Automation

The foundation of a fast close is eliminating manual data gathering and consolidation. This requires integrated systems where transactions automatically flow into the accounting platform. Expense management, bill payment, and revenue recognition tools should feed the general ledger directly. Automated bank feeds should import and categorize transactions daily. API connections should link the CRM and accounting system for revenue data, and HRIS integration should handle payroll recording automatically.

For many companies, this means upgrading from entry-level QuickBooks to a mid-market system like NetSuite, Sage Intacct, or Xero. One client spending $85,000 annually on accounting staff time for manual close processes invested $28,000 in system upgrades and integrations. Within six months, close time had dropped by 12 days per month, and one full-time equivalent was reassigned from data gathering to strategic analysis.

Element 2: Continuous Accounting

Traditional close assumes all transactions are recorded at month-end. Continuous accounting means recording transactions throughout the month so that the close becomes verification rather than data entry. Specific practices include daily bank reconciliation, which takes 10 minutes per day compared to three hours at month-end, weekly accounts receivable and accounts payable reviews, mid-month preliminary review to catch errors before they compound, continuously updated accrual tracking, and daily revenue recognition for subscription businesses.

Element 3: Standardized Close Checklist

Fast, reliable close requires standardized processes that do not depend on individual knowledge or memory. Every close optimization engagement should produce a detailed checklist specifying every task required, the responsible person for each task, expected completion timelines, task dependencies, and approval requirements. The checklist typically includes 40 to 60 distinct tasks organized chronologically across the five-to-seven-day close window. Task management tools such as Asana, Monday, or Trello enable collaborative tracking so everyone knows what is pending and what is blocking progress.

Element 4: Reconciliation Discipline

Reconciliation delays kill close schedules. Non-negotiable standards must be established:

- All accounts reconcile to zero each month, with no unreconciled items rolling forward

- Reconciliations must be completed within the first two to three days of close

- Any reconciliation discrepancy over $500 requires documented investigation and explanation

- Items unresolved for 60 or more days must be escalated to the controller or the CFO immediately

Element 5: Pre-Close Activities

Significant work can happen before month-end, substantially reducing the post-close burden. Standard pre-close practices include a final-week expense submission deadline requiring all employee expenses submitted by the 25th, accounts payable clearing for all invoices that have arrived and been approved, commission calculation and preliminary approval based on near-final results, preliminary revenue review for companies with complex recognition requirements, and accrual schedule updates for all known items before month-end arrives.

Element 6: Technology-Enabled Reporting

Final reporting should not require three to five days of manual Excel work. Modern accounting systems enable automated generation of standard profit and loss statements, balance sheets, and cash flow reports. One client built a comprehensive board reporting package that previously required more than 20 hours monthly to compile manually. After implementing reporting automation, the package was auto-generated from their accounting system in two hours, with four additional hours of CFO time for strategic commentary. The quality was higher, the data was more current, and the finance team recaptured 16 hours every single month.

Close Optimization: Before vs. After Results

| Metric | Before Optimization | After Optimization | Improvement |

| Days to close | 18–22 days | 6–8 days | 65–70% faster |

| Rework rate (journal entries) | 20–30% | Under 5% | 4–6x improvement |

| Manual reporting hours | 20+ hours/month | 2–4 hours/month | 80% reduction |

| Reconciliation completion | Partial / deferred | 100% on-time | Full compliance |

| Strategic analysis time | 10 days/month | 23 days/month | 130% more time |

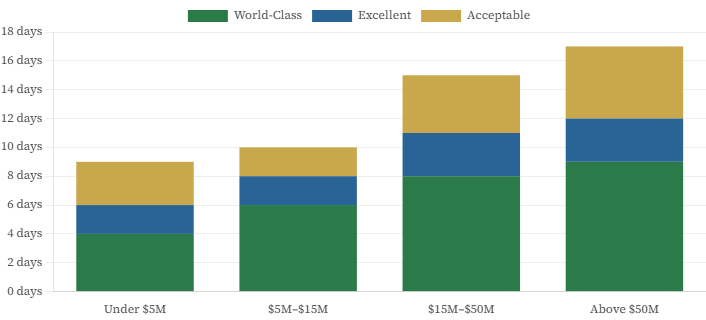

Close Performance Benchmarks by Company Size

Close timing targets vary by company size, complexity, and systems maturity.

For companies under $5M in revenue with straightforward operations, meaning a single entity, domestic only, and a simple revenue model, 5 to 7 business days is achievable with good processes and basic system integration. Under 5 days is possible with sophisticated automation, but it is generally not worth the investment at this scale.

For companies between $5M and $15M with moderate complexity, such as multiple entities, recurring revenue, or multiple products and services, 7 to 10 business days is good performance. Five to 7 days is excellent and requires continuous accounting practices combined with solid systems integration.

For companies between $15M and $50M with significant complexity, including international operations, multiple subsidiaries, or complex revenue recognition, 10 to 12 business days is acceptable. Seven to 10 days is good performance and requires mid-market systems at the NetSuite or Sage Intacct level.

For companies above $50M, 10 to 15 days is the norm. Seven to 10 days is a strong performance. Under 7 days is world-class and is typically achieved only by public companies with SEC reporting timelines that demand extreme speed.

Close Speed Benchmarks by Company Size

| Revenue Range | Slow (Problem) | Good Performance | Excellent | World-Class |

| Under $5M | 15+ days | 7–10 days | 5–7 days | Under 5 days |

| $5M – $15M | 12+ days | 7–10 days | 5–7 days | Under 5 days |

| $15M – $50M | 15+ days | 10–12 days | 7–10 days | Under 7 days |

| Above $50M | 20+ days | 10–15 days | 7–10 days | Under 7 days |

Key Performance Indicators for Measuring Close Quality

To optimize close, it must be measured consistently. The following metrics form the foundation of close performance management.

- Days to close measures calendar days from the month-end to finalized, approved financials. Ten or more days is slow. Seven to 10 days is good. Five to 7 days is excellent. Under 5 days is world-class

- Days to preliminary close measures days from the month-end to preliminary statements ready for management review, target preliminary statements available within 60% of the total close day count

- Rework rate measures the percentage of journal entries or reports requiring correction after initial creation target under 5%

- Reconciliation completion rate measures the percentage of required reconciliations completed on schedule without deferral. The target is 100% on-time, every period

- Close variability measures the standard deviation of close timing month over month. A close that takes 7 days reliably is more valuable than one that occasionally hits 5 days but regularly runs to 12

The Business Impact of a Fast Close

The value of close optimization extends far beyond the accounting department.

When leadership has 5-day-old financial data instead of 20-day-old data, they make decisions based on current reality. A 15-day improvement in close speed enables three to four additional strategic decision cycles per quarter, allowing faster response to market changes, margin deterioration, competitive threats, or growth opportunities.

Issues caught in 5 days are dramatically easier to resolve than issues discovered 20 days later. If project margins are deteriorating, identifying the problem in early February enables correction before quarter-end. Identifying it in late February means the damage is already fully reflected in results, and quarterly conversations with clients or stakeholders become reactive rather than proactive.

When financial results are available quickly, operational leaders can connect their decisions to outcomes in real time. Sales compensation analysis 5 days after quarter-end enables productive conversations about quota attainment and pipeline coverage. The same analysis 25 days later, feels irrelevant because everyone is already focused on the new quarter.

One client reduced the close from 18 days to 6 days over four months. The CFO estimated that faster close enabled three strategic decisions per quarter that would previously have been delayed: pricing changes that improved gross margins by 3%, hiring timeline adjustments that reduced recruiting costs by $15,000, and project staffing optimization that improved utilization by 8%. The financial impact from improved decision-making quality exceeded $200,000 annually, which was far more than the total cost of the close optimization engagement.

Common Close Optimization Mistakes to Avoid

The Technology-Only Approach. Some companies spend $50,000 or more on new accounting software and achieve minimal improvement because they have not fixed underlying process problems. Technology enables a fast close, but only when processes are sound. Fix the process first, then implement technology that supports efficient processes. Never do it the other way around.

The “We’ll Do That Next Month” Syndrome. Close optimization requires the discipline to implement new practices even when they are initially unfamiliar and feel slower. Teams frequently implement changes for one month, struggle with the new process, and revert to old approaches until there is time to do it right. This prevents any sustainable improvement. Commit to a minimum three-month implementation timeline where the new processes are non-negotiable, even when they initially take longer.

Reconciliation Deferral. When close deadlines approach, teams sometimes skip reconciliations or mark items to be investigated later in order to hit timing targets. This creates accumulating problems that eventually cause catastrophic close failures. A 10-day close with all reconciliations complete is always preferable to a 7-day close with mounting unreconciled items building toward a future crisis.

The Solo Optimization. Controllers who attempt to optimize close without involving the broader team face resistance and struggle to maintain new approaches. Effective optimization requires team involvement in designing the changes and a genuine shared commitment to the improvement goal. Involving an experienced fractional CFO provides the strategic guidance, implementation framework, and organizational authority that makes adoption stick.

Fractional CFO services are typically structured as hourly rates, monthly retainers, or project-based fees. Most growing companies access fractional CFO expertise for 25 to 40% of the $180,000 to $300,000 annual commitment a full-time CFO requires, with no equity, benefits, or long-term employment obligations. For close optimization specifically, most engagements run $8,000 to $15,000 over three to four months, with a return on investment that typically pays back within the first quarter of improved performance.

—

FAQ

How do we reduce close time without sacrificing accuracy or taking shortcuts that create problems later?

This concern is entirely valid—we never advocate sacrificing quality for speed. The key insight is that slow close processes are often inaccurate because of their manual, inconsistent nature. Fast, automated close processes are typically more accurate because they reduce manual data entry and consolidation that creates errors. Specifically, optimization improves accuracy through: systematic processes that ensure nothing gets skipped (close checklists catch forgotten adjustments that manual processes miss), automation that eliminates transcription errors (data flowing automatically from source systems to GL eliminates the “I mistyped this number” errors), continuous accounting that catches errors when they’re fresh (reconciling daily means you remember the transaction; reconciling 30 days later requires forensic investigation), and required reconciliations that can’t be skipped (slow close processes often defer reconciliations “until later”; fast close requires all reconciliations complete before financials are approved). The way to reduce close time safely is through systematic improvement over 3-6 months, not aggressive one-time cuts. Month 1, implement close checklist and measure current timing. Month 2, implement continuous reconciliation processes (daily bank recs, weekly AR/AP review). Month 3, implement system integrations eliminating manual data gathering. Month 4, implement accrual automation and prepaid expense tracking. Each month, you improve process without compromising quality. We also recommend maintaining quality checks throughout optimization: controller or CFO should review financials with increased scrutiny during first 3 months of new close process to catch any errors quickly, compare month-over-month trends in key accounts to identify unusual variances that might signal errors, maintain reconciliation discipline absolutely—never defer reconciliations to hit close timelines, and conduct quarterly external review by fractional CFO or advisor to ensure quality hasn’t degraded. One client implemented aggressive close optimization reducing timing from 17 days to 8 days in 2 months. Quality metrics showed error rate increasing from 3% to 11% of journal entries requiring correction. We slowed the pace, focused on training and systematization, and reached 7-day close with 2% error rate over the following 3 months. Sustainable optimization preserves quality while improving speed.

Our accounting team is already overwhelmed—how can we add close optimization work on top of current responsibilities?

This catch-22 is real: teams consuming 20 days monthly on close don’t have time to optimize close, but without optimization they’ll remain overwhelmed indefinitely. We resolve this through structured approach that actually reduces workload during implementation. First, recognize that close optimization is an investment—you invest 15-20 hours in process improvement this month to save 40 hours every subsequent month. Calculate the ROI and commit leadership support for the upfront investment. Second, phase implementation to avoid overwhelming the team. Month 1: just document current process and create close checklist (8-10 hours investment). Month 2: implement continuous bank reconciliation only (5 hours setup, then 10 minutes daily—net time savings within 2 weeks). Month 3: implement one system integration eliminating the most time-consuming manual process. Each phase delivers time savings that creates capacity for the next phase. Third, get external help during implementation. A fractional CFO or accounting consultant can handle implementation heavy-lifting—selecting and implementing systems, building processes, training team—while internal team maintains current operations. This external investment (typically $8K-15K over 3-4 months) accelerates implementation and prevents internal team burnout. Fourth, consider temporary accounting support during implementation. Bring in part-time contractor for 2-3 months to handle routine transactions while internal team focuses on optimization. This $5K-8K investment prevents implementation from derailing current operations. Fifth, secure management buy-in for close timeline extension during implementation. If close normally takes 15 days, plan for 18-20 days during month 1-2 of optimization while team learns new processes. This flexibility prevents panic and shortcuts that undermine implementation. Finally, celebrate quick wins. After implementing bank rec automation that saves 2 hours monthly, explicitly acknowledge “this is working—we’re making progress.” This builds momentum and team confidence in the improvement process. One client with overwhelmed 2-person accounting team was skeptical they could optimize while maintaining current close. We brought in fractional CFO 1 day per week for 4 months ($12K total) who handled implementation while internal team maintained operations. By month 5, close time had reduced from 20 days to 9 days, creating 22 hours monthly of recovered capacity. The team described it as “the first time in 3 years we’re not constantly behind.” The implementation investment had 4-month payback through reduced stress and overtime.

What’s realistic to expect for close timing based on company size and complexity, and when should we consider our close “good enough”?

Close timing benchmarks vary by company size, complexity, and systems sophistication, but we’ve established general guidelines. For companies under $5M revenue with straightforward operations (single entity, domestic only, simple revenue model): 5-7 business days is achievable with good processes and basic accounting system integration. Under 5 days is possible with sophisticated automation but probably not worth the investment at this scale. For companies $5-15M revenue with moderate complexity (multiple entities, recurring revenue, multiple products/services): 7-10 business days is good performance. 5-7 days is excellent and requires continuous accounting practices plus good systems. For companies $15-50M revenue with significant complexity (international operations, multiple subsidiaries, complex revenue recognition): 10-12 business days is acceptable. 7-10 days is good and requires sophisticated systems (NetSuite/Intacct level). Under 7 days is excellent and typically requires enterprise-grade systems and dedicated accounting operations focus. For companies $50M+ revenue: 10-15 days is the norm. 7-10 days is good. Under 7 days is world-class (achieved by public companies with SEC reporting requirements demanding speed). These timelines assume quality isn’t compromised—if you can close in 5 days but with 12% error rate requiring material revisions, that’s not success. The “good enough” threshold depends on business needs rather than industry benchmarks. Ask: how quickly do we need financial data to make good decisions? If leadership makes major decisions monthly in week 1 of the new month, 7-day close delivers timely data. If decisions happen quarterly, 15-day close might suffice. Are we preparing for transaction (fundraising, M&A)? Buyers expect 10-day or faster close as indicator of operational maturity. If preparing for exit, close speed matters more than if planning to operate independently for 5+ years. Do we have investor/lender reporting requirements? Some credit agreements require monthly financials within 15 days; others allow 30 days. Your close must beat the reporting deadline. Is accounting team capacity constrained? If you have 1 person handling accounting for $8M company, 12-day close might be realistic limit without adding staff. Rather than pursuing arbitrary benchmarks, optimize to the point where close timing stops being a business constraint. If leadership is happy with financial data timeliness, accuracy is high, and accounting team isn’t overwhelmed, you’ve achieved “good enough” even if theoretically faster close is possible.

Further Reading

Browse more articles in the CFO Pro+Analytics Knowledge Base for in-depth financial frameworks, models, and strategies tailored to your business.

Ready to take action? Explore our Fractional CFO Services → to see how we partner with founders and operators to build financial clarity.