The Role of a Fractional CFO in Risk Management

TL;DR: Most companies treat risk management as compliance theater—documenting risks nobody acts on and building contingency plans nobody updates. We’ve found that effective risk management isn’t about predicting disasters but about building organizational resilience through systematic identification, quantification, and mitigation of threats to business value. Companies with active fractional CFO-led risk management recover from adverse events 60% faster and suffer 40% smaller financial impact than those with passive risk frameworks. The difference isn’t better prediction; it’s better preparation and faster response when risks materialize.

The Risk Nobody Saw

Two years ago, we worked with a professional services firm generating $12M in annual revenue. They had risk documentation (required for their insurance), quarterly risk committee meetings, and a detailed risk register listing 27 identified risks. On paper, they looked sophisticated.

Then their largest client—representing 32% of annual revenue—was acquired by a competitor. The new parent company immediately terminated the relationship, citing conflict of interest. The termination was effective in 30 days per contract terms.

The firm had identified “client concentration risk” in their risk register. The documented mitigation was “diversify client base over time.” But they’d taken no concrete action. They hadn’t established concentration thresholds that triggered specific responses. They hadn’t built contingency plans for rapid client loss. They hadn’t created financial reserves adequate to weather major revenue disruption.

Within 60 days, they’d laid off 22 of 48 employees, surrendered their office lease early (paying $85,000 in breakage fees), and depleted cash reserves to $23,000. They survived only because the CEO personally guaranteed a $200,000 line of credit. What should have been a manageable setback became existential crisis because risk “management” had been documentation without action.

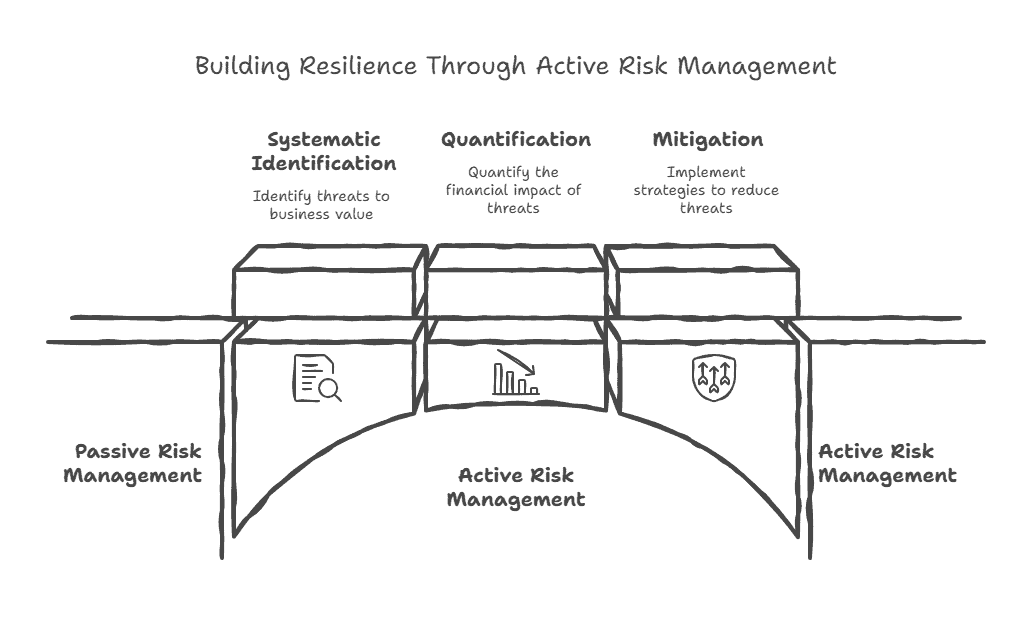

Creating a resilient workplace environment requires proactive risk management, shaping organizational culture, and implementing safety protocols that go beyond documentation to foster operational excellence and long-term growth.

The tragedy is this was entirely preventable. If they’d established that no client should exceed 20% of revenue and actively managed concentration, they would have diversified before crisis hit. If they’d maintained financial reserves equal to 6 months of fixed costs, they could have weathered the transition. If they’d built pipeline specifically to backfill potential concentration risk, they would have had opportunities ready when the loss occurred.

This pattern repeats constantly. Companies document risks without quantifying them. They identify threats without building specific mitigation plans. They create contingency plans without resourcing them or testing them. Then when risks materialize, they scramble reactively rather than executing prepared responses.

The Fractional CFO Framework for Risk Management

We’ve developed a systematic approach to risk management that transforms it from compliance exercise into strategic capability. This framework enables companies to build resilience without becoming paralyzed by fear.

Risk management frameworks such as ISO 31000, COSO ERM, and NIST have evolved over decades, shaped by extensive experience and industry best practices. Fractional teams help tailor these established practices to the unique needs and scale of smaller organizations.

Phase 1: Systematic Risk Assessment and Identification

Effective risk management starts with comprehensive identification of threats to business value. We conduct this through structured analysis across five categories:

Strategic Risks: Threats to business model viability—competitive disruption, technology shifts, market changes, regulatory evolution, or customer preference changes. For a subscription software company, strategic risks might include emergence of free open-source alternative, shift from per-user to consumption pricing industry-wide, or major platform vendor entering their market.

Operational Risks: Disruptions to business operations—supply chain failures, key person dependencies, facility problems, technology outages, or process breakdowns. A manufacturing company faces supplier bankruptcy, equipment failure, quality control failures, or facility damage from natural disasters.

Financial Risks: Threats to financial stability—cash flow disruptions, credit availability, currency fluctuations, interest rate changes, or credit concentration. A company with international operations faces currency risk; a company with floating-rate debt faces interest rate risk; a company with limited banking relationships faces credit access risk.

Compliance and Legal Risks: Regulatory violations, contract breaches, litigation exposure, IP infringement, or compliance failures. Companies in regulated industries face enforcement actions; companies with complex contracts face dispute risk; companies with valuable IP face infringement or misappropriation risk.

Reputational Risks: Events that damage brand or stakeholder trust—product failures, service quality problems, leadership misconduct, data breaches, or negative publicity. B2C companies face social media crises; B2B companies face reference customer problems; all companies face cybersecurity and data protection risks.

We identify risks through facilitated workshops with leadership, interviews with functional leaders, analysis of historical near-misses and incidents, and review of industry-wide failure patterns. Company leadership plays a critical role in recognizing when external risk leadership support is needed and ensuring that risk management aligns with strategic oversight and governance. The goal is comprehensive identification without becoming paralyzed by possibility.

Phase 2: Risk Quantification and Prioritization

Not all risks deserve equal attention. We quantify risks along two dimensions: likelihood and impact.

Likelihood Assessment: What’s the probability this risk materializes in the next 12-24 months? We use five-point scales: very low (<10% probability), low (10-30%), moderate (30-50%), high (50-70%), very high (>70%). These probabilities come from historical data where available, industry experience, and informed judgment.

Impact Assessment: If this risk materializes, what’s the financial and strategic damage? We quantify impact in financial terms: revenue loss, cost increase, cash consumption, and business disruption duration. A client concentration risk that loses 30% of revenue creates $3.6M annual impact for a $12M company. Cybersecurity breach might cost $200K in immediate response plus $500K in long-term customer loss.

Risk Prioritization Matrix: Plotting likelihood against impact creates a prioritization framework. High likelihood, high impact risks demand immediate attention and significant mitigation investment. Low likelihood, low impact risks may not warrant mitigation beyond awareness. The most interesting quadrant is low likelihood, high impact—”catastrophic but unlikely” risks that merit contingency planning even if mitigation isn’t cost-effective.

For the professional services firm, client concentration risk was high likelihood (acquisitions happen frequently), high impact ($3.8M revenue loss). This should have been their #1 priority risk. Instead, they focused attention on lower-impact, lower-likelihood risks because they seemed more manageable.

Phase 3: Mitigation Strategy Development

Once risks are quantified, we develop specific mitigation strategies that reduce either likelihood or impact. Establishing formalized procedures for safety, regular assessments, and cybersecurity is essential to ensure effective risk mitigation and data protection.

Likelihood Reduction: Actions that make risks less likely to occur—diversifying suppliers (reduces supply chain risk), redundant systems (reduces technology outage risk), compliance audits (reduces regulatory risk), or quality programs (reduces product defect risk). These strategies often require ongoing investment but prevent problems before they occur.

Impact Reduction: Actions that reduce damage when risks materialize—insurance (transfers financial impact), financial reserves (provides buffer), backup facilities (enables faster recovery), or contract protections (limits exposure). These strategies accept that risks may occur but limit consequences.

Risk Transfer: Shifting risk to third parties through insurance, contracts, hedging, or partnerships. Insuring against property damage transfers risk to insurer. Currency hedging transfers foreign exchange risk to counterparty. Outsourcing transfers operational risks to vendor (though creates vendor risk).

Risk Acceptance: For some risks, cost of mitigation exceeds benefit. These risks are explicitly accepted with eyes open. A $2M company probably can’t afford business interruption insurance covering all scenarios—they accept some risk of disruption. The key is making acceptance explicit rather than defaulting into it through inaction.

For client concentration risk, likelihood reduction means actively managing to diversification targets: no client over 20% of revenue, no industry over 40% of revenue, top 5 clients not exceeding 55% of revenue. Impact reduction means maintaining financial reserves equal to 6 months fixed costs and building sales pipeline with 4x coverage to enable rapid backfill if major client is lost.

Phase 4: Contingency Planning

For high-priority risks, we build specific contingency plans defining response actions if risks materialize. These plans answer: What early warning indicators signal the risk is materializing? What immediate actions do we take when risk occurs? Who has authority to activate the plan? What resources (financial, operational) do we need? How do we communicate with stakeholders?

For major client loss, contingency plan might include: early warning indicators (acquisition rumors, relationship quality deterioration, budget cuts), immediate actions (activate top 10 prospect blitz, implement temporary expense reduction targeting 15% opex cut, draw credit line to ensure liquidity), authority (CEO can activate plan without board approval for speed), resources ($250K in financial reserves allocated specifically to this contingency), and communication (prepared talking points for remaining clients and employees addressing the situation).

We test contingency plans through tabletop exercises where leadership walks through the scenario and execution. This reveals gaps and builds muscle memory so execution isn’t purely theoretical.

Phase 5: Monitoring and Review

Risks evolve as business, market, and external conditions change. Effective risk management includes ongoing monitoring and periodic review.

Key Risk Indicators (KRIs): Establish metrics that signal when specific risks are increasing. For client concentration, monthly monitoring of top client percentage, top 5 client percentage, and client pipeline development. For financial risk, weekly monitoring of cash position, credit utilization, and DSO trends. When KRIs cross thresholds, investigation and response trigger automatically.

Quarterly Risk Reviews: At least quarterly, review the complete risk register: Have new risks emerged? Have existing risks changed in likelihood or impact? Are mitigation strategies working? Do contingency plans need updates? These reviews prevent risk registers from becoming stale documentation that doesn’t reflect current reality.

Post-Event Analysis: When risks materialize or near-misses occur, conduct thorough analysis: What happened? Why did it happen? Were early warnings missed? Did mitigation strategies work? What needs to change? This learning cycle continuously improves risk management capability.

Common Risk Management Failures

Through hundreds of engagements, we’ve identified risk management failures that repeat across companies and industries.

The Documentation Theater: Companies create impressive risk registers, hold quarterly risk committee meetings, and produce risk reports—but nobody acts on the analysis. Risks are documented but not mitigated, contingency plans are written but not resourced, and risk “management” becomes compliance checkbox rather than business discipline. Real risk management changes behavior and resource allocation, not just documentation.

The Optimism Bias: Leadership teams systematically underestimate likelihood and impact of risks because acknowledging threats feels uncomfortable or pessimistic. They rate high-likelihood risks as moderate, high-impact risks as moderate impact, and assume “it won’t happen to us.” This bias causes under-investment in mitigation until crisis forces recognition. We combat this through outside perspective and historical data on how frequently risks actually materialize.

The Mitigation-Free Zone: Some companies identify and quantify risks thoroughly but never develop mitigation strategies. They know concentration risk exists but don’t set diversification targets. They recognize cybersecurity threats but don’t invest in defenses. They understand key person risk but don’t cross-train or document knowledge. Risk identification without mitigation is awareness without action.

The Contingency Illusion: Others build contingency plans that look impressive on paper but can’t be executed practically. Plans require resources that don’t exist, assume response times that aren’t realistic, or depend on authorities that aren’t clear. When crisis hits, these plans are abandoned immediately as impractical. Real contingency plans must be executable within actual organizational constraints.

A robust fractional risk management framework empowers organizations with the confidence to make assured and decisive strategic choices, fostering trust in their growth and resilience.

The Role of the Fractional CFO in Risk Management

Fractional CFOs bring specific capabilities that make risk management more effective. Organizations can benefit from hiring a fractional chief, such as a Fractional Chief Risk Officer (fractional CRO), to provide strategic risk management leadership on a flexible, cost-effective basis.

Financial Quantification: CFOs translate qualitative risks into financial impact—moving from “client concentration is concerning” to “losing our top client would reduce revenue by $3.8M and require $850K in restructuring costs.” This quantification enables rational prioritization and decision-making about mitigation investment.

Scenario Modeling: CFOs build financial models showing business impact under different risk scenarios. What happens to cash flow, profitability, and runway if key risk materializes? These models inform contingency planning and reserve adequacy decisions.

Independent Perspective: Fractional CFOs aren’t operationally invested in current approaches, enabling objective risk assessment. They can challenge “we’ve always done it this way” thinking and push for mitigation when operations teams resist change.

Board Communication: CFOs translate risk management into language that boards and investors understand, ensuring governance level awareness and oversight rather than risk management remaining siloed in operations.

Financial Discipline: CFOs ensure that risk mitigation gets resourced—that contingency plans have actual financial backing, that insurance coverage is adequate, and that mitigation investments happen rather than getting perpetually deferred.

Strategic Oversight: A fractional chief or chief risk executive brings part-time, yet strategic, oversight and consulting tailored to organizational needs. By leveraging fractional CRO services, companies gain access to executive-level risk management and governance expertise without the cost of a full-time hire.

Competitive Advantage: Leveraging fractional risk leadership enables businesses to differentiate themselves through superior risk management and safety initiatives, creating a competitive advantage and strengthening long-term market positioning.

Staff Augmentation and Support

In my CFO travels, I’ve watched too many growing companies get blindsided by risks they never saw coming—and it’s rarely the obvious ones that cause the damage. Consider one of my manufacturing clients who sailed through their financial audits year after year, only to face a $2.3 million regulatory fine because they missed a single compliance requirement buried in new environmental regulations. The reality is that today’s business environment throws an expanding arsenal of risks at companies: financial volatility that can swing 15-20% quarter-over-quarter, operational disruptions that cost an average of $84,000 per hour of downtime, compliance failures that carry penalties averaging $14.8 million per violation, and cyber threats that hit 43% of small businesses annually. Most organizations I work with lack the specialized expertise to manage these risks effectively—especially when new threats and regulatory requirements emerge faster than they can hire and train internal teams.

This is where staff augmentation through fractional risk management becomes not just valuable, but essential for survival. Here’s how it works: instead of the $180,000+ annual commitment of a full-time risk manager (plus benefits, equity, and infrastructure costs), you bring in expert guidance and additional resources on a flexible basis—typically 15-30 hours per month at a fraction of the cost. What’s particularly fascinating is how quickly this approach fills capability gaps. One of my retail clients implemented fractional risk management and identified $400,000 in operational risk exposure within the first 60 days—exposure that would have cost them significantly more to remediate after the fact rather than prevent proactively.

The sophistication extends to companies that need proactive risk management but don’t require a permanent, in-house risk team—which describes roughly 70% of the mid-market companies I consult with. Through staff augmentation, business leaders gain access to specialized expertise across financial risk assessment (including scenario modeling that can predict cash flow impacts within 3-5% accuracy), compliance program development, operational risk analysis, and information security frameworks. This enables organizations to not just identify existing risks, but to respond to market changes with agility and implement mitigation strategies that align precisely with their growth trajectory. The compound effect? Companies using this approach typically see 40-60% fewer risk-related surprises and maintain stakeholder confidence even during periods of rapid scaling.

Building Organizational Risk Culture

Technical risk management frameworks fail without supportive organizational culture. We work with leadership to build environments where:

Risk Discussion Is Normal: Teams regularly discuss “what could go wrong” without being labeled pessimistic or negative. Risk awareness is seen as professional prudence, not organizational weakness.

Risk Owners Are Clear: Every identified risk has a designated owner responsible for monitoring and mitigation. Ownership isn’t diffused across committees but assigned to specific individuals with accountability.

Near-Misses Are Learning Opportunities: When risks almost materialize, the organization treats it as valuable learning rather than relief that “nothing bad happened.” These near-misses often provide clearer warnings than actual incidents.

Mitigation Is Funded: Risk mitigation competes for resources alongside growth investments, and leadership explicitly evaluates risk-reduction ROI. A $50K investment in redundant systems that prevents $500K outage risk is viewed as high-return investment, not discretionary expense.

Plans Are Tested: Contingency plans get exercised through tabletop simulations or limited tests, ensuring they’re executable rather than theoretical.

The companies with strongest risk management aren’t those with the longest risk registers or most sophisticated documentation. They’re companies where risk awareness is embedded in decisions, mitigation is resourced, contingencies are prepared, and response capability is tested.

—

FAQ

How do we determine how much to invest in risk mitigation without becoming paralyzed by fear or wasting resources on unlikely threats?

This tension between under-investing (leaving exposure) and over-investing (consuming resources on unlikely events) is central to effective risk management. We use cost-benefit analysis to establish rational mitigation investment levels. The framework: multiply risk probability by financial impact to calculate expected loss, then compare mitigation cost to expected loss reduction. For example, a risk with 15% annual probability and $800K impact has expected annual loss of $120K. If mitigation costing $40K annually reduces probability to 3%, the benefit is reduction in expected loss from $120K to $24K—a $96K benefit for $40K cost. Clear positive return. However, some mitigations have poor cost-benefit ratios. Insuring against very unlikely but catastrophic events might cost $30K annually for 1% probability of $1.2M loss—$30K cost to reduce expected loss from $12K to $0. Poor financial return, though might still be rational if catastrophic loss would threaten business survival. We generally follow these guidelines: for high-likelihood, high-impact risks (top priority quadrant), invest aggressively in mitigation even if cost approaches expected loss—these risks threaten core business and merit premium spending. For high-impact, low-likelihood risks (catastrophic but rare), focus on contingency planning and selective transfer (insurance) rather than expensive likelihood reduction. For low-impact risks regardless of likelihood, mitigation spending should be minimal—accept these risks or implement low-cost controls. One useful heuristic: mitigation should generally cost 20-40% of annual expected loss for good cost-benefit ratio. A risk with $200K annual expected loss might justify $40K-80K in mitigation spending. Beyond that, you’re over-investing relative to the threat. This framework enables rational discussion: “This mitigation costs $100K annually to address a $30K expected loss—that’s over-investing. Let’s find a lower-cost approach or accept the risk.” The goal isn’t zero risk; it’s optimal risk-adjusted resource allocation.

Our business has so many potential risks that systematic management seems overwhelming—how do we start without getting paralyzed?

The paralysis concern is legitimate—comprehensive risk identification can produce 50+ identified risks, making systematic management feel impossible. We prevent this through deliberate focus and staged implementation. Start with the critical few, not the comprehensive many. In initial risk assessment, identify the top 5-7 risks ranked by expected loss (probability × impact). These high-priority risks get full treatment: quantification, mitigation strategies, contingency plans, monitoring, and quarterly review. Lower-priority risks get documented but remain on the watch list rather than active management. This focused approach makes risk management tractable while addressing threats that actually matter. One client initially identified 43 distinct risks across their business. Rather than trying to manage all 43, we focused on the 6 with highest expected losses: client concentration ($180K expected annual loss), key person risk ($140K), cybersecurity ($95K), supplier concentration ($70K), credit facility renewal ($55K), and regulatory changes ($45K). These six risks represented 75% of total expected losses, so focusing on them captured most of the benefit. The other 37 risks stayed documented but weren’t actively managed beyond annual review. Eighteen months later, after successfully mitigating or building contingencies for the top 6, they elevated the next tier for active management. Stage implementation over time. Month 1: identify and quantify risks, prioritize top 5-7. Month 2: develop mitigation strategies for #1-2 risks. Month 3: build contingency plans for high-impact risks. Month 4: implement monitoring systems and KRIs. Month 5-6: execute mitigation strategies and establish review rhythms. This staged approach prevents overwhelming the organization while making steady progress. Use templates and frameworks to reduce custom work for each risk. Create standardized contingency plan formats, risk assessment templates, and mitigation strategy frameworks that can be quickly customized rather than built from scratch. We’ve developed templates that reduce contingency plan development from 8-10 hours to 2-3 hours per risk. Finally, remember that risk management doesn’t require perfection. A simple risk register with the top 5 risks quantified, basic mitigation strategies defined, and quarterly reviews scheduled is infinitely better than no risk management. Start there, demonstrate value, then expand sophistication over time.

How do we get leadership teams to take risk management seriously when there’s always pressure to focus on growth and current operations?

This challenge is nearly universal—risk management competes for attention against immediate operational demands and exciting growth initiatives. Several approaches increase leadership engagement. First, speak in financial language that resonates with business leaders. Instead of “we face supplier concentration risk,” say “single-source supplier relationships create 22% probability of $450K disruption if supplier fails—$99K expected annual loss that should be mitigated.” Quantification makes risks concrete rather than abstract. Second, connect risk management to strategic objectives rather than positioning it as separate activity. If strategic goal is achieving profitability, show how financial risks threaten that objective. If goal is enterprise market expansion, show how security and compliance risks block enterprise sales. Frame risk management as enabling strategy rather than competing with it. Third, use near-misses and close calls as teachable moments. When competitor experiences breach, major client churns, or market disruption occurs, conduct immediate review: “Could that happen to us? What would the impact be? How are we protected or exposed?” These real-world events make risks tangible in ways that hypothetical scenarios don’t. Fourth, require risk analysis for major decisions rather than making it separate process. When evaluating market expansion, acquisitions, or major investments, systematically include risk assessment in decision framework. This makes risk management integral to decision-making rather than background activity. Fifth, establish clear governance with board oversight. When board/investors ask quarterly “What are our top risks and how are we managing them?”, leadership takes it seriously. Board-level risk committees or regular risk review in board meetings elevate importance. Sixth, demonstrate ROI through case studies and evidence. Show that companies with active risk management recover from disruptions 60% faster. Quantify the value of avoided losses through mitigation: “Our investment in backup suppliers cost $35K but prevented $180K in losses when our primary supplier had quality failures.” Finally, start small with quick wins. Identify one high-visibility risk, implement mitigation, show results. Success builds credibility for broader risk management adoption. One client struggled with leadership engagement until their largest client threatened to churn over service quality issues. We implemented systematic account health monitoring and proactive issue escalation for top clients. Within 6 months, they’d prevented two additional major client issues through early intervention. Quantifying $890K in retained revenue created immediate credibility, and leadership began requesting risk assessment for other areas. Sometimes it takes small demonstration of value before leadership fully invests in systematic practice.

Further Reading

Browse more articles in the CFO Pro+Analytics Knowledge Base for in-depth financial frameworks, models, and strategies tailored to your business.

Ready to take action? Explore our Fractional CFO Services → to see how we partner with founders and operators to build financial clarity.