How a Fractional CFO Manages Board Communications

Board and investor communication failures rarely announce themselves loudly. They build quietly through missed expectations, inconsistent messaging, and slowly eroding confidence until the damage suddenly surfaces as a failed fundraise, unwanted board interference, or a founder being replaced. For growing companies, these failures are often avoidable with the right financial leadership in place.

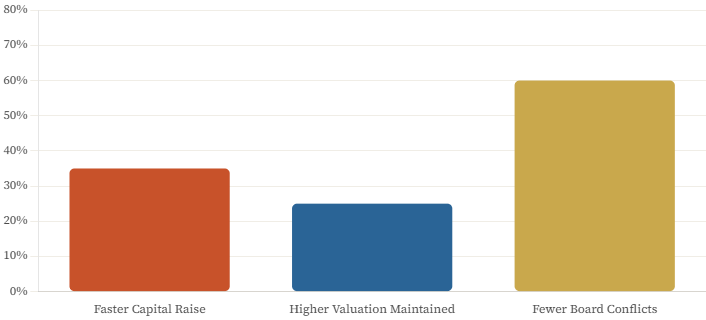

A fractional CFO provides exactly that leadership, without the $180,000–$250,000 annual overhead of a full-time hire. Companies with fractional CFO-led investor relations raise capital 35% faster, maintain 25% higher valuations, and experience 60% fewer board conflicts than those where founders manage communications directly. The difference is not a better spin. It is systematic transparency, consistent messaging, and the financial credibility that sophisticated stakeholders demand.

What Boards and Investors Actually Need

Understanding what boards and investors need starts with recognizing that they each carry distinct responsibilities and therefore require different types of information.

Board governance: Board members have fiduciary duties. They need to confirm the company is not running out of cash, identify risks early, evaluate executive performance through objective metrics, and provide guidance on major strategic decisions like acquisitions, pricing changes, or market expansion. To fulfill these duties effectively, they need comprehensive financial statements, variance analysis with clear explanations, forward-looking cash runway forecasts, and documented risk assessments.

Lead investors with board seats: These stakeholders receive full board packages, monthly updates, and expect to be consulted on major decisions. They are active partners in strategy, not passive observers.

Participating investors without board seats: Typically entitled to quarterly updates focused on high-level performance and material developments. They are financially interested but operationally distant.

Angel investors and small shareholders usually receive annual updates unless they are participating in a new round. Ignoring them entirely creates friction during fundraising when you need their approval and support.

Stakeholder Communication Requirements

| Stakeholder Type | Update Frequency | Content Depth | Consultation Level |

| Board Members | Monthly + Quarterly | Full financials, variance analysis, risk assessments | Major strategic decisions |

| Lead Investors (Board Seats) | Monthly | Full board packages, KPIs, forecasts | Active strategy partners |

| Participating Investors | Quarterly | High-level performance, material developments | Financially interested only |

| Angel / Small Shareholders | Annual | Summary updates | New round participation only |

At the core of all these relationships is the confidence equation: consistent messaging, accurate forecasting, and demonstrated operational competence. Destroy any one element and the relationship degrades. Tell investors you are on track in January, and miss badly in March, and confidence collapses. Project 18 months of cash runway and announce an emergency bridge at month eight, credibility is gone. Promise a Q2 product launch and deliver in Q4, and stakeholders stop believing in your execution.

A Real Example: The Board Meeting That Changed Everything

Consider a Series A SaaS company that had achieved 40% year-over-year revenue growth. By most measures, the business was performing well. But in a board meeting, a member asked a simple question: “What is your burn multiple?”

The CEO did not know the answer. When pressed for a cash runway, he estimated around 18 months but could not provide specifics. When asked about unit economics, he referenced CAC payback but used definitions that had shifted from previous meetings. When questioned about why Q2 burn had exceeded forecast by $200,000, there was no variance analysis to explain it.

The board called an emergency follow-up meeting. Three board members independently contacted a CFO candidate they had previously recommended. The message was clear: bring in professional financial leadership or face consequences.

The company had not committed fraud or hidden serious problems. They had simply failed to manage board communications professionally. Revenue growth was real, but without financial context, numbers meant nothing. The CEO’s inability to answer basic financial questions signaled either incompetence or evasiveness. Neither builds confidence.

After rebuilding their board communications structure, the transformation was substantial:

- Monthly investor updates with consistent KPI definitions replaced sporadic crisis-driven emails

- Quarterly board packages delivered five days before meetings replaced rushed last-minute presentations

- Within two quarters, board meetings shifted from tense interrogations to productive strategic conversations

The Fractional CFO Framework for Investor Relations

A well-structured investor relations framework is built around three core components: monthly updates, quarterly board packages, and proactive variance communication.

Monthly Investor Updates

For lead investors and board members, monthly updates prevent surprises at quarterly meetings. A well-structured monthly update includes an executive summary covering key wins, key challenges, key metrics, and key decisions. It also includes a financial dashboard showing revenue, burn rate, cash balance, and runway, followed by operational KPIs across sales, customers, product, and team, and a brief progress update on major strategic initiatives.

Format consistency matters as much as content. Use the same KPI definitions, the same dashboard layout, and the same structure every month. Inconsistency makes trend analysis impossible and suggests the business lacks systematic tracking. Updates should go out within 10 days of the month-end. Sending preliminary numbers on day five that get revised on day fifteen destroys credibility faster than sending final numbers on day ten.

Quarterly Board Packages

Board meetings require comprehensive packages delivered five to seven days in advance. This allows board members to review materials, formulate informed questions, and use the meeting itself for discussion and decision-making rather than information downloading.

A complete quarterly board package should include a one-page executive summary covering quarter highlights and key decisions needed, full financial statements with prior quarter and prior year comparisons, budget variance analysis for items exceeding 10% deviation, a KPI dashboard showing trends over four to six quarters, strategic initiative progress against annual plans, and a forward-looking forecast for the next four quarters with any assumption changes clearly noted.

One practical improvement that consistently improves board meeting quality is transitioning from dense slide-heavy presentations to concise advance packages. A company that moved from 60-slide presentations delivered during two-hour meetings to 15-page advance packages with a 10-slide discussion deck reported that decisions requiring two to three previous meetings were routinely resolved in single sessions.

Variance Analysis and Expectation Management

The most important board communication is not celebrating wins. It explains misses before they become surprises. When forecast variance exceeds 10% in either direction, proactive communication must explain:

- What specifically drove the variance — not vague references to “market conditions” but named deals and specific expense categories

- Whether the variance is a timing issue or a permanent change

- What actions are being taken in response

- How forecasts have been updated going forward

Boards generally tolerate misses when they are explained with context and paired with a plan. A statement like “We are tracking 15% below forecast due to three enterprise deals slipping to Q4, we have updated the forecast and accelerated mid-market activity to partially offset” maintains trust. Reporting significantly below the forecast without any explanation destroys it.

Common Board Communication Failures to Avoid

The surprise negative: Companies that hide bad news, hoping to fix problems before the board notices, consistently make things worse. Board members eventually discover problems through back-channel conversations, customer references, or independent financial analysis. A hidden problem discovered through external channels destroys trust far more than a proactively disclosed challenge paired with an action plan.

Moving goal posts: Changing KPI definitions or success metrics between meetings triggers suspicion. If you report monthly recurring revenue in Q1 and switch to annual contract value in Q2 without explanation, board members question whether you are masking deteriorating metrics. When definition changes are genuinely necessary, explain them clearly and restate historical periods under the new definition.

Data-free updates: Presenting board updates built entirely on stories and anecdotes without supporting data raises questions about whether anyone is actually tracking the business. Customer success stories are valuable, but they need to be supported by NPS scores, retention data, and revenue metrics. Execution stories need delivery timelines and measurable outcomes.

Defensive posture: When board members ask difficult questions, responding defensively damages relationships. Boards exist specifically to ask hard questions. When questions feel unfair, that is usually a communication failure, not a board failure. Respond with data. “Our top client represents 18% of revenue, down from 28% last year. We have a policy capping any single client at 15%, and here is the eight-quarter trend showing concentration declining.” This demonstrates competence rather than resistance.

Board Communication Failure vs. Best Practice

| Communication Failure | What Happens | Best Practice |

| Hiding bad news | Board discovers through back channels — trust collapses | Proactively disclose with an action plan |

| Moving goalposts (changing KPIs) | Triggers suspicion of masking declining metrics | Explain changes and restate historical data |

| Data-free updates | Board questions whether business is actually tracked | Support every story with NPS, retention, revenue data |

| Defensive responses | Damages board relationships and signals evasiveness | Respond with data and demonstrate competence |

Strategic Decision Frameworks That Boards Respect

Beyond regular reporting, boards provide guidance on major strategic decisions. Effective fractional CFO communication frames these decisions with financial analysis that enables genuine discussion rather than vague debate.

When presenting a major decision such as market expansion, an acquisition, or a significant hire, the framework should clearly define the options being considered (not just “should we expand to Europe” but Option A: no expansion, Option B: hire a UK country manager, Option C: full European rollout), the financial implications of each option including required investment, expected return, break-even timeline, and sensitivity to key assumptions, the risks and proposed mitigations for each path, and a recommendation with clear, data-backed rationale.

This structured approach transforms board conversations. Instead of debating whether European expansion “makes sense,” the discussion becomes whether an $800,000 investment with an 18-month payback in the base case and a 24-month payback in the conservative case is attractive given the company’s current cash position and other capital priorities. That is the kind of discussion that produces useful decisions.

The Specific Role of the Fractional CFO in Board Relations

Fractional CFOs bring distinct capabilities to board and investor relationships that founders typically do not possess, not because founders lack intelligence, but because financial credibility is built through experience and context that takes years to develop.

Financial credibility: Board members trust CFO-prepared financial packages in ways they may not trust founder-assembled decks. The format, terminology, and level of analytical rigor signal whether someone understands financial governance.

Objective perspective: CFOs can deliver difficult messages with less emotional attachment than founders. “We need to cut burn by 25%” or “this acquisition does not make financial sense” lands differently when delivered by an experienced financial officer.

Pattern recognition: Fractional CFOs working across multiple companies recognize which metrics boards consistently scrutinize, which questions reliably arise, and which warning signs trigger concern. This pattern recognition allows them to address issues proactively rather than reactively.

Package preparation: CFOs own board package preparation, ensuring consistent quality and on-time delivery without consuming founder bandwidth. This frees founders to focus on strategic positioning rather than financial assembly.

Meeting management: During board meetings, CFOs handle financial questions in real time, provide on-the-spot analysis, and enable deeper strategic conversation by managing the tactical financial details that otherwise derail high-level discussion.

Building Long-Term Board Partnership

The goal of board communications is not compliance. It is a partnership. Companies that treat board updates as box-checking exercises eventually have boards that behave like auditors. Companies that treat board members as genuine strategic assets develop relationships that add meaningful value beyond capital.

Proactive engagement: Rather than only communicating when information is required, engage board members on strategic questions before decisions are finalized. “We are evaluating a pricing change and would value your perspective before we finalize,” signals partnership rather than oversight.

Individual relationships: Beyond formal meetings, fractional CFOs build individual relationships with board members through informal check-ins and targeted conversations. These relationships enable more candid exchanges and better problem-solving outside the formal board context.

Feedback loops: Periodically ask board members whether the current communication format meets their needs and what they would like to see changed. This demonstrates commitment to effective governance and often surfaces simple improvements that meaningfully strengthen the relationship.

Crisis communication: When genuine crises occur, such as a major customer loss, key executive departure, or product failure, immediate board notification is essential. The framework is straightforward: notify the board immediately, provide an initial assessment within 24 hours, deliver an action plan within 48 to 72 hours, and give regular updates until the issue is resolved. Boards can tolerate almost any business crisis if they are kept informed and see competent management responding. What they cannot tolerate is discovering a crisis through a third party.

The Measurable Impact of Professional Investor Relations

The business case for fractional CFO-led investor relations is not theoretical. Businesses preparing for fundraising with robust financial frameworks in place complete due diligence cycles 23% faster. Companies with disciplined communication strategies raise follow-on capital 67% faster and maintain higher valuations during market downturns because investors understand the underlying business fundamentals, not just the quarterly headlines.

One SaaS company raised $3.2 million against a $3.1 million target, within 3% of their goal, largely because transparent reporting systems had built immediate investor confidence during diligence. A manufacturing client was able to explain working capital fluctuations clearly enough to close a Series B round that had previously stalled due to investor confusion about the company’s cash dynamics.

Beyond fundraising, the compounding benefit of consistent, credible communication is that investor relationships become strategic assets rather than recurring stress points. Investors who trust your financial reporting become advisors, connectors, and advocates. Investors who doubt your numbers become adversaries.

Conclusion

Effective board and investor communications are not about presenting the best version of reality. They are about building the systematic transparency that allows stakeholders to trust what they are seeing, ask productive questions, and make informed decisions alongside management.

Fractional CFOs bring the financial credibility, process discipline, and pattern recognition needed to transform investor relations from a quarterly obligation into a genuine competitive advantage. Companies that invest in this infrastructure raise capital faster, maintain stronger valuations, and build board relationships that accelerate growth rather than constrain it.

If your board meetings still feel more like interrogations than strategic partnerships, the issue is rarely bad board members. It is almost always inconsistent communication, a missing financial context, or a lack of systematic preparation. Those are solvable problems, and solving them begins with the right financial leadership.

Further Reading

Browse more articles in the CFO Pro+Analytics Knowledge Base for in-depth financial frameworks, models, and strategies tailored to your business.

Ready to take action? Explore our Fractional CFO Services → to see how we partner with founders and operators to build financial clarity.