My First 30 Days as Your Fractional CFO

in Fractional CFO, Accounting and Finance, Cash Flow Improvement, CFO, CFO Services, Finance, Financial Modeling, Fractional CFO, All Posts

When I step into a new engagement, my focus is on identifying quick wins that create immediate value. Once we succeed in these critical areas, we build momentum and continue to improve systematically. The first 30 days aren’t about grand transformation; they’re about establishing the financial foundation that makes everything else possible.

TL;DR: First, establish a clean and reliable source of truth so decisions are based on consistent data. Then, confront cash directly by defining burn, runway, and actual liquidity. From there, validate the business model by examining unit economics in detail. Finally, document how the business runs so that execution no longer depends on institutional memory.

The Philosophy Behind the First 30 Days

The first month of a fractional CFO engagement isn’t about reinventing your business or pitching a five-year strategic vision. It’s about conducting a forensic, unsentimental audit of where you are right now. Through my work at tirabassi.com, I’ve learned that effective financial management is fundamentally about removing ambiguity. The first 30 days are when we identify every place where ambiguity has masqueraded as “the way we’ve always done it.”

This approach is particularly critical for emerging technology companies and AI-driven businesses where rapid growth often outpaces operational discipline. The companies that scale successfully are those that build financial clarity into their foundation rather than trying to retrofit it later.

Four Critical Audits That Drive Quick Wins

1. The “Source of Truth” Audit: Establishing Data Integrity

Before analyzing any numbers, I examine the systems that produce them. If your financial infrastructure is compromised, every decision based on that data is built on unstable ground. I start by asking: where does this data originate, and how reliable is the journey from transaction to report?

In many mid-sized firms, particularly fast-growing tech companies, financials become a patchwork of QuickBooks entries, manual Excel spreadsheets, and sales team estimates. My first audit focuses on General Ledger (GL) hygiene and data consistency.

The Critical Questions:

- Are transactions categorized consistently across periods?

- Does month-end close actually happen by a specific date, or do entries drift in for weeks afterward?

- Can we trace any number in a management report back to its source transaction?

- Are automated integrations between systems creating data inconsistencies?

The Management Implication: If your chart of accounts and categorization methods are inconsistent, no amount of strategic vision can produce reliable insights. I audit the chart of accounts to ensure it reflects how your business actually generates and consumes cash, not just how your bookkeeper prefers to organize receipts.

Common Findings: In SaaS companies, I frequently discover revenue recognition issues where cash collection is confused with earned revenue. In marketplace businesses, I often find that platform fees, payment processing costs, and refunds aren’t consistently categorized, distorting gross margin calculations.

The Quick Win: Establishing a single source of truth allows leadership to make decisions confidently, knowing the underlying data is reliable. This typically takes 7-10 days but pays dividends for years.

2. The “Burn and Runway” Check

I’m consistently surprised by how many founders operate on a general sense of their runway rather than precise numbers. In finance, imprecision is a precursor to crisis.

I perform a rigorous analysis of cash-on-hand versus true, unavoidable burn. This isn’t simply reviewing the P&L, it’s examining the calendar, understanding payment timing, and identifying every dollar commitment you’ve made.

Net Burn vs. Gross Burn Analysis: I distinguish between your gross burn (total cash out) and net burn (cash out minus cash in). More importantly, I separate fixed costs that aren’t moving—payroll, rent, debt service, critical software subscriptions—from variable expenses that could be reduced if necessary.

The Accounts Receivable (AR) Aging Audit: If your revenue is sitting in an unpaid invoice from 90 days ago, it’s not revenue—it’s an interest-free loan you’ve extended to your customer. I audit exactly who owes you money, how much, when payment was due, and what the actual (not the polite) reason is for the delay.

The Accounts Payable (AP) Analysis: Equally important is understanding what you owe and when. I’ve seen companies celebrate improved cash positions only to discover they’ve simply delayed vendor payments, creating a time bomb of upcoming obligations.

Cash Flow Forecasting: I build a 13-week cash flow forecast that shows exactly when money comes in and goes out. This granular view often reveals patterns that monthly P&L statements mask—like the timing mismatch between when you pay commission and when you collect the associated revenue.

The Quick Win: Knowing your true runway with precision allows you to make strategic decisions from a position of knowledge.

3. Unit Economics: The “Is This Actually a Good Business?” Test

You can generate $10 million in revenue and still be building a fundamentally unprofitable business if your unit economics don’t work. I dive deep into the relationship between what it costs to acquire and serve a customer versus the profit they actually generate.

Many companies mask these issues with aggregate metrics. Leadership will tell me, “Our gross margins are healthy at 65%.” But when I audit the actual variable costs—payment processing fees, customer support hours, cloud infrastructure costs that scale with usage, shipping and fulfillment—that “healthy” margin often contracts significantly.

The Forensic Approach: I select three to five representative customers or transactions from the last quarter and trace every single dollar spent to acquire and service them. This micro-audit usually reveals macro-truths about pricing strategy, cost structure, and which customer segments actually drive profitability.

For SaaS Companies:

- Customer Acquisition Cost (CAC): What’s the fully-loaded cost including marketing, sales salaries, software tools, and the time required to close and onboard?

- Lifetime Value (LTV): What does a customer actually pay over their entire relationship, accounting for churn, expansion, and contraction?

- LTV:CAC Ratio: Is it above 3:1? If not, why not, and what’s the path to improving it?

For Marketplace Businesses:

- Take rate economics: After payment processing, customer support, and fraud prevention, what’s left?

- Contribution margin by transaction type: Which transaction types actually subsidize which others?

For Product Businesses:

- Landed cost of goods: What does the product actually cost including shipping, returns, and payment processing?

- Customer service costs: How much does it cost to support a typical customer through their lifecycle?

The Quick Win: Understanding which customers, products, or services generate profit allows you to double down on what works and fix or eliminate what doesn’t.

4. The “Institutional Memory” Audit: Documenting Critical Processes

This audit examines people and processes, specifically looking for “key person dependencies”—places where critical tasks get done only because one person happens to know how.

The Process Walkthrough: I ask team members to walk me through standard processes like billing, payroll, revenue recognition, or month-end close. If they can’t describe the process without saying “it depends” or “I just know when something looks wrong,” we’ve identified a vulnerability.

What I’m Looking For:

- Processes stored in people’s heads rather than documented systems

- Critical tasks that only one person can perform

- Informal workarounds that have become permanent solutions

- Manual processes that could be automated

- Knowledge that would walk out the door if a key employee left

Documentation Standards: I don’t just want to know that a process exists—I want to know it can be executed consistently by different people with the same results. This means documented procedures, checklists, and quality controls.

The Quick Win: Transforming institutional knowledge into documented, repeatable systems reduces risk, enables scaling, and improves consistency.

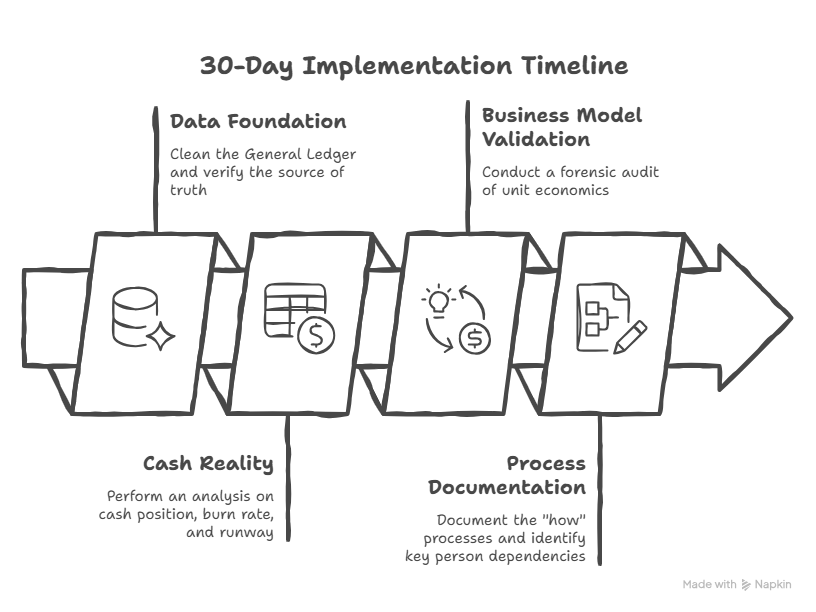

The 30-Day Implementation Timeline

Week 1: Data Foundation Clean the General Ledger and verify the source of truth. Identify and stop data leaks. Establish consistent categorization and ensure month-end close processes are reliable.

Week 2: Cash Reality Perform an analysis on cash position, burn rate, and runway. Face the bank balance honestly. Build a 13-week cash flow forecast and AR/AP aging analysis.

Week 3: Business Model Validation Conduct a forensic audit of unit economics. Verify that customer acquisition and service delivery is actually profitable at the unit level. Identify which segments drive real value.

Week 4: Process Documentation Document the “how” processes. Transform institutional memory into repeatable, scalable systems. Identify and begin addressing key person dependencies.

What Comes After the First 30 Days

The initial audit creates clarity, but the real work is using that clarity to drive improvement. In months two and three, we typically focus on:

- Building recurring financial reporting rhythms that provide consistent visibility

- Implementing process improvements identified during the audit

- Developing financial models that support strategic decision-making

- Creating board-ready materials that tell your financial story clearly

- Establishing KPI tracking that aligns with business model economics

The first 30 days establish the foundation. Everything that follows builds on that foundation to create a financial operation that drives strategic value rather than simply recording history.

Frequently Asked Questions

Q: Isn’t 30 days too fast to start making significant changes?

I’m not attempting to change your culture or business model in 30 days—I’m clearing the windshield so you can see the road. You can’t make informed strategic decisions if you can’t see your current position clearly. These audits provide the visibility required to make any meaningful change at all. Think of it as establishing a baseline truth before optimization.

Q: What’s the biggest red flag you encounter in these initial audits?

Defensiveness. When I ask why a particular expense is elevated or why a process works a certain way, an emotional justification rather than a data-driven explanation tells me exactly where management discipline needs development. The best clients respond to audit findings with curiosity (I didn’t realize that—let’s fix it) rather than defensiveness (that’s just how we’ve always done it). Financial operations should be optimized continuously, not defended emotionally.

Q: What if the audit reveals the business is in worse shape than the CEO thought?

That’s actually the most valuable outcome possible. Discovering problems during a structured audit with a plan to address them is infinitely better than discovering them during a cash crisis or failed fundraising round. Knowing you’re lost is the first step toward getting found. I’ve never seen a company harmed by facing financial reality; however, I’ve seen many harmed by avoiding it until options narrow significantly.

Salvatore Tirabassi is a fractional CFO and founder of CFO Pro+Analytics, helping founder-owned and famfounderinesses build the financial infrastructure to grow, delegate, and exit on their terms.

Assess your CFO needs in 5-minutes

“`

For more on this topic, read our driver-based forecasting vs the numbers you trust and building a 3-statement financial model for forecasting.