How a Fractional CFO Prepares a Business for Due Diligence

Due diligence failures kill more deals than valuation disagreements. Companies with fractional CFO-led due diligence preparation close transactions 40% faster and maintain 15 to 20% higher valuations than those scrambling to respond to buyer requests. The difference is not having perfect financials. It has organized, credible data with clear narratives that build buyer confidence rather than raising concerns. Effective preparation transforms due diligence from a defensive interrogation into an offensive demonstration of business quality, turning skeptical acquirers into confident buyers.

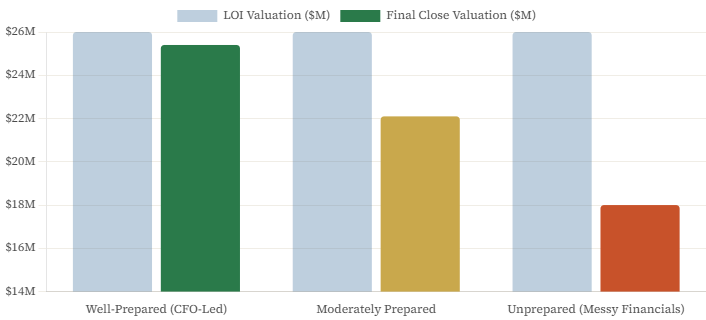

The $4 Million Valuation Haircut: What Poor Preparation Actually Costs

Last year, I worked with a SaaS company that had received a letter of intent from a strategic acquirer at 6.5x revenue, a $26M valuation on $4M ARR. The founder was celebrating what seemed like a life-changing exit. Then due diligence began.

Within the first week, serious problems surfaced. The company could not cleanly reconcile revenue recognized in its accounting system to actual customer payments. Three years of financial statements showed different revenue figures than what had been reported to the board. Customer contracts had inconsistent terms that made churn analysis unreliable. Several enterprise customers listed in their sales materials were still on free trials.

Each discovery triggered additional questions. Each question revealed more inconsistencies. Each inconsistency eroded buyer confidence. The acquirer’s tone shifted from enthusiasm about the acquisition to uncertainty about what they were actually buying.

Sixty days into diligence, the acquirer returned with a revised offer: $18M purchase price with $3M held in escrow pending resolution of revenue recognition issues. That was effectively an $11M reduction from the original letter of intent. The founder accepted because the deal had already been announced internally, key employees had been notified, and returning to business as usual was no longer realistic. They lost $8M in value that had been built over seven years, not because the financials were fraudulent, but because they were messy. Messy financials in due diligence create the same fear as intentional misrepresentation.

This pattern repeats constantly. Companies operate with good enough financial systems in private, then discover that what works for running the business does not survive rigorous external scrutiny. They spend the first 30 days of diligence scrambling to create documentation that should have existed all along.

What Due Diligence Actually Examines

Due diligence is not one process. It is multiple parallel investigations by different functional teams, all trying to validate assumptions and uncover risks.

Financial Due Diligence

Quality of earnings analysis is the centerpiece. Buyers scrutinize revenue recognition policies, expense timing, non-recurring items, and working capital changes. They are looking for aggressive revenue recognition, understated expenses, or one-time benefits that make performance look better than it is. They reconstruct normalized or adjusted EBITDA by removing non-recurring items and correcting accounting policies they view as overly aggressive.

Revenue validation traces revenue from contracts to invoices to cash receipts to accounting entries. Diligence teams verify that what is recognized as revenue actually represents completed transactions with real cash collection behind them. They examine customer concentration, churn rates, contract terms, and any revenue recognition complexities such as multi-element arrangements or deferred revenue.

Working capital analysis examines accounts receivable aging, inventory quality and turnover for product businesses, accounts payable aging, and deferred revenue obligations. Buyers calculate working capital requirements and determine how much cash the business will need post-transaction.

Historical financial analysis covers three years of financials analyzed for trends, seasonality, margin evolution, and consistency. Buyers want to understand whether current performance represents sustainable business fundamentals or a temporary peak.

Operational Due Diligence

Operational diligence validates that the business model works as described and can continue operating after the transaction closes.

- Customer analysis validates customer counts, examines churn by cohort, analyzes concentration risk, and verifies that key customer relationships belong to the company rather than to the founder personally

- For technology companies, technical diligence examines code quality, scalability, technical debt, security practices, and IP ownership

- Sales and marketing validation examines customer acquisition costs, sales pipeline quality, sales cycle length, and marketing effectiveness

Legal and Compliance Due Diligence

Legal diligence identifies legal risks, contractual obligations, and compliance issues that could create post-closing liabilities. Every material contract gets reviewed: customer contracts, vendor agreements, employment agreements, leases, loans, and partnership agreements. Buyers look for unusual terms, change-of-control provisions that could be triggered by the acquisition, or commitments that create unexpected obligations.

Due Diligence Areas and Key Risk Factors

| Diligence Area | Primary Focus | Common Red Flags | Impact on Valuation |

| Quality of Earnings | Revenue recognition, EBITDA normalization | Aggressive recognition, large adjustments | High — can reduce 15–30% |

| Revenue Validation | Contract-to-cash traceability | Missing contracts, free trials counted as customers | High |

| Customer Analysis | Churn, concentration, founder dependency | Top 3 clients = 60%+ ARR | Moderate–High |

| Technical Diligence | Code quality, IP ownership, scalability | Unassigned IP, high technical debt | Moderate |

| Legal / Contracts | Material obligations, change-of-control | Non-standard terms, verbal agreements | Variable |

The Six-Month Preparation Timeline

Effective due diligence preparation does not happen in the weeks before a transaction. It requires months of systematic work. For companies planning fundraising or an exit, a six-month preparation timeline is the standard we recommend.

Months 5 and 6: Financial Foundation

The first priority is ensuring the last three years of financial statements are accurate, consistent, and would survive external audit scrutiny. This means proper revenue recognition, complete expense accruals, accurate balance sheet reconciliations, and consistent accounting policies applied across all periods. If revenue recognition approaches or accounting treatments have changed, restate historical periods for consistency before going to market.

The second priority is restructuring the chart of accounts to support the analysis buyers will conduct. Create clear revenue categories by product or service line and customer segment. Structure expense categories to distinguish the cost of goods sold from selling, general, and administrative expenses clearly.

If the business is running on basic QuickBooks at $5M or more in revenue, consider upgrading to a more sophisticated system. Buyers view accounting system sophistication as a proxy for operational maturity. Moving to NetSuite, Sage Intacct, or a comparable mid-market system signals professional operations and enables the detailed reporting that diligence requires.

Months 3 and 4: Documentation and Organization

Customer contracts are among the most commonly problematic areas in diligence. Review all customer contracts and move toward standard terms wherever possible. Non-standard terms create diligence complexity and raise concerns about hidden obligations. If you have 50 customers with 50 different contract structures, buyers worry. Standardize renewal terms, pricing terms, termination provisions, and service level agreements.

Begin building the virtual data room during this phase. Organize documents into the structure buyers will expect: financials including monthly profit and loss statements, balance sheets, and cash flow statements for 36 months; all material contracts; corporate documents including formation docs, bylaws, board minutes, and the capitalization table; and operational materials including sales pipeline data, customer metrics, product roadmap, and marketing analytics.

Reconcile any disconnects between data sources during this phase. If your CRM shows different customer counts than your accounting system, identify why and fix it before buyers ask.

Months 1 and 2: Narrative Development and Testing

Conduct an internal quality of earnings analysis, identifying non-recurring items, accounting policy choices, and adjustments that buyers will question. Prepare explanations for these items proactively. If you capitalized $200,000 in software development costs in a way that could be questioned, identify it upfront with a clear rationale rather than defending it reactively when challenged.

Develop a comprehensive management presentation explaining your business model, market opportunity, competitive positioning, unit economics, growth strategy, and financial performance. Engage advisors to conduct mock due diligence 45 to 60 days before going to market. This exercise reveals missing documentation, data inconsistencies, and narrative weaknesses while you still have time to address them.

Building the Due Diligence Narrative

Having clean data is necessary but not sufficient. Due diligence requires telling a compelling story that makes buyers confident in the acquisition.

The Growth Story

Buyers want to understand what drives growth and whether it is sustainable. The narrative needs to explain which customer segments are growing fastest and why, which acquisition channels are most effective and scalable, how retention and expansion economics support the growth rate, and what investments are required to maintain the trajectory.

Rather than stating that the company is growing 40% year over year, a credible narrative sounds like this: mid-market companies in healthcare and financial services with 50 to 200 employees have an 18-month customer acquisition cost payback period, 92% annual retention, and 115% net dollar retention. Specificity is what makes a growth story credible. Vague claims invite skepticism. Specific, data-backed assertions with clear logic invite confidence.

The Profitability Path

For companies burning cash, buyers need confidence in the path to profitability. The narrative should show current unit economics, the path to positive unit economics if currently negative, the operational leverage model showing how margins improve with scale, required investment to reach profitability, and the timeline to cash flow breakeven.

The Risk Mitigation Story

Every business has risks. Rather than obscuring them, effective diligence preparation requires acknowledging risks proactively and demonstrating clear mitigation strategies.

For customer concentration, the largest customer represents 18% of ARR. Policy has been established that no single customer should exceed 15%, and active diversification is underway. The top five customers represent 42% of ARR, down from 58% two years ago.

Proactive risk acknowledgment with clear mitigation demonstrates management sophistication. It actually increases buyer confidence rather than raising additional concerns.

Common Due Diligence Failures That Kill Deals

Through dozens of transactions, the same preparation failures appear repeatedly. Understanding them in advance is the most effective way to avoid them.

The Revenue Recognition Time Bomb: Many companies recognize revenue when they should not, or use inconsistent approaches across periods. For SaaS companies, recognizing the full annual contract value upfront rather than ratably over the subscription term is the classic mistake. Buyers will force revenue recognition policy corrections that can reduce historical revenue by 15 to 30%, which destroys the growth story that justified the valuation in the first place.

The Adjusted EBITDA Credibility Problem: Companies that present adjusted EBITDA by removing large amounts of expenses as non-recurring or one-time expenses lose credibility quickly. If $800,000 is being adjusted out of $1.2M of reported EBITDA, buyers question whether the business is profitable at all. Adjustments should be limited to genuinely non-recurring items backed by clear documentation for each adjustment.

Incomplete Customer Contracts: Missing customer contracts, inconsistent terms, or verbal agreements create significant problems in diligence. If a company claims $4M ARR but can only produce contracts documenting $3.1M, buyers will value the business based on the documented amount. Every missing contract erodes credibility and valuation. Complete contract documentation for every customer representing more than 2% of revenue is a non-negotiable preparation requirement.

Founder Dependency: When customer relationships, product knowledge, and key decisions all reside with the founder personally, buyers worry about post-acquisition continuity. Effective preparation demonstrates systematic operations that can continue without founder involvement. Document key processes, develop the leadership team, and ensure that business success is demonstrably systematic rather than personality-driven.

Virtual Data Room Structure

| Folder | Key Documents Required | Priority Level |

| Financial | Monthly P&L (36 months), bank reconciliations, AR/AP aging, revenue by segment | Critical |

| Contracts | All customer contracts (>2% revenue), vendor agreements, and employment agreements | Critical |

| Corporate | Formation docs, board minutes, cap table, option plan | Critical |

| Operational | Customer metrics, sales pipeline, product roadmap, org chart | High |

| Legal & Compliance | IP assignments, litigation history, data privacy docs, insurance | High |

Managing Active Diligence After the Letter of Intent

Once a letter of intent is signed, the 45 to 90-day active diligence period begins. This period determines whether the deal closes and at what price.

Response speed matters more than most sellers expect. The faster information requests are answered, the faster diligence concludes, and the less time buyers have to develop concerns or expand scope. Targeting 24 to 48-hour response times for all reasonable requests is the standard. Delayed responses create the impression that something is being hidden or that the organization lacks capability.

Consistency across all responses is critical. Every answer must be consistent with previous answers and consistent with materials in the data room. Inconsistency triggers investigation spirals that delay deals and reduce trust at exactly the moment when trust is most valuable.

Scope management is equally important. Buyers will request extensive information, some of it reasonable and some of it excessive. Transaction counsel should help determine which requests are standard and which represent overreach. Being cooperative on legitimate diligence needs while pushing back professionally on unreasonable requests is a skill that experienced fractional CFOs develop through repeated transaction exposure.

Finally, maintaining business focus during a 60 to 90-day diligence process is essential. Companies that become so consumed by diligence that business performance deteriorates create new buyer concerns during the process. Allocating approximately 10 to 15 hours weekly to diligence response with clear boundaries protecting operational focus is the discipline that keeps both the deal and the business on track.