Improving Cash Collections in SaaS

Cash collections separate SaaS companies that survive from those that do not. Most founders focus on bookings and revenue while cash sits uncollected in accounts receivable, failed credit card charges, and customer disputes. The difference between a 30-day and a 60-day collection cycle can mean months of runway. Build systematic collection processes, automate dunning for failed payments, negotiate payment terms that favor your cash position, and treat accounts receivable management as strategically important as sales. Every dollar collected faster is a dollar that extends the runway and reduces dilution.

Why Cash Collections Matter More Than Revenue

Every month, SaaS companies celebrate revenue growth while their cash position quietly deteriorates. A business closes $200,000 in new ARR, recognizes $16,700 in monthly revenue, and the cash has not arrived and will not for 45 days because of payment terms and customer delays. Meanwhile, the burn rate is $150,000 monthly, and the runway is shrinking. The revenue number looks strong. The bank account tells a different story.

This gap between revenue recognition and cash collection kills companies. Revenue exists on the income statement when it is earned, typically when service is delivered. Cash exists when it lands in the bank account. For SaaS companies with undisciplined collections, these two events can be months apart.

Companies with disciplined collections operate with 15 to 25-day average collection cycles. Companies with poor collections stretch to 45 to 60 days. On a $2M ARR business, the difference between a 20-day and a 50-day collection cycle is $165,000 in working capital trapped in receivables instead of sitting in the bank. That is a month of runway sitting in accounts receivable. The industry average for SaaS collections cycles typically falls in the 40 to 45-day range, meaning that improving collections meaningfully can put a business well ahead of standard performance while freeing up significant cash.

DSO Benchmarks by Company Type

| Company Type | Target DSO | Typical DSO (Poor) | Working Capital at Risk |

| SMB (Card-based billing) | Under 5 days | 15–25 days | Low |

| Mid-Market (Invoice billing) | 20–30 days | 45–60 days | Moderate |

| Enterprise (Net-30 terms) | 30–35 days | 50–70 days | High |

| Industry Average (SaaS) | 20–25 days | 40–45 days | $165K per $2M ARR |

Understanding Your Collection Cycle: Days Sales Outstanding

Days Sales Outstanding measures how long it takes to collect payment after invoicing. Calculate it monthly by dividing accounts receivable by monthly revenue divided by 30 days.

If accounts receivable total $100,000 and monthly revenue is $150,000, DSO is 20 days. That means payment is being collected an average of 20 days after invoicing, which is strong performance.

Track DSO monthly without exception. If it is rising, the problem exists before it becomes a crisis. DSO moving from 25 days to 40 days over six months means customers are paying more slowly, payment failures are increasing, or the AR team is not following up with enough consistency. These patterns are fixable when caught early and very expensive when caught late.

Segment DSO by customer type to understand where the problem lives. Enterprise customers on net-30 terms should show DSO around 30 to 35 days, accounting for the small percentage who pay late. SMB customers on automated credit card billing should show a DSO under 5 days. If enterprise DSO is running above 50 days, there are systematic issues with large customer collections that need direct attention.

Track aging buckets to see how long invoices have been outstanding: current at 0 to 30 days, 31 to 60 days, 61 to 90 days, and 90 days or more. Anything over 60 days needs aggressive collection action. Anything over 90 days carries a high risk of never being collected.

The B2B Invoice Collection Process

The companies with the best collection rates have this process automated and consistently enforced.

- Send the invoice on day one, with clear payment terms stated explicitly on the document

- On day 15, send a friendly reminder: payment is due in 15 days. Here are the payment options

- On day 30, when payment is due, send a firm notice: payment was due today and has not been received

- On day 35, call the customer directly — do not email — call the accounts payable contact and confirm the invoice is in their queue

- On day 45, send a formal demand: payment is 15 days overdue, service will be suspended in 5 business days without payment

- On day 50, suspend service and send a final notice before collections escalation

This process should run through a CRM or billing system with automated reminders. Account managers should receive alerts when their customers hit 35 days overdue. The finance team should review aging reports daily and prioritize the oldest receivables. Customers who know these steps will be followed through consistently tend to pay on time. Customers who learn there are no real consequences for late payment do not.

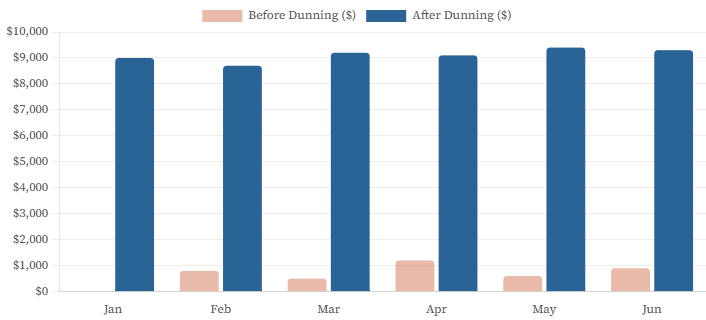

Automating Collections for Card-Based Billing

For SaaS companies with automated card billing, the collection challenge is different: catching and recovering failed payments before they become involuntary churn.

Credit cards fail at 5 to 15% monthly rates, depending on the customer mix. Cards expire, hit spending limits, get flagged by fraud detection systems, or simply have insufficient funds. Most SaaS companies treat failed charges as automatic churn. Companies with disciplined collections treat them as recovery opportunities.

Build a dunning workflow with these steps. On day zero, when the card charge fails, retry immediately. This catches temporary declines from fraud detection algorithms or daily spending limits. On day one, send an email alert to the customer with a direct link to update their payment method. On day three, retry the card charge. Many temporary issues, including fraud holds and spending limit resets, resolve within 72 hours. On day seven, send a second email with firmer language. On day ten, make the final retry and send the final notice. On day fourteen, cancel or permanently suspend the subscription.

This process recovers 50 to 70% of failed payments that would otherwise churn without any human intervention. One client was losing $15,000 monthly to failed payments with no systematic follow-up. After implementing proper dunning, they recovered $9,000 of that amount consistently every month. That is $108,000 annually that was available the entire time and simply not being collected.

Use tools like Stripe Smart Retries, Churn Buster, or the built-in dunning functionality of your billing platform. Do not manually chase failed card payments. Automate the process entirely and reserve human effort for high-value recovery situations.

Negotiating Payment Terms That Favor Cash Flow

Early-stage SaaS companies often accept whatever payment terms enterprise customers request. Net-60 terms get agreed to. Quarterly payments for annual contracts are agreed to. This destroys cash flow in ways that take months to show up and years to fix.

Negotiate aggressively for terms that favor the company’s cash position from the start. Annual prepayment is the gold standard. Offer a 10 to 15% discount for customers who pay the full annual contract upfront, and push every customer toward this structure. The discount reduces short-term revenue recognition, but the cash flow benefit is substantial. A customer paying $10,000 upfront is a better cash outcome than a customer paying $12,000 in quarterly installments, especially when the runway is tight and capital is expensive.

Push for net-15 instead of net-30 on invoiced accounts. Many customers will accept shorter payment terms without negotiation if net-15 is presented as the standard. Reducing collection time by 15 days across the customer base compounds significantly at scale.

For enterprise customers who insist on paying by credit card, add a 2.5% processing fee to cover the cost of delayed cash and card processing fees. This either moves customers to faster payment methods or recovers the carrying cost of slower cash.

Require automatic payment, either card or ACH, for all month-to-month contracts. Monthly customers should never be on invoice billing. Eliminate the collection cycle for these accounts entirely.

For large implementation projects before recurring revenue begins, negotiate milestone-based payment structures: 30% upfront, 30% at the first defined milestone, and 40% at completion. Do not finance customer implementations from company cash. The company’s capital is too expensive for that.

Improving average cash collection timing by 20 or more days through better contract negotiation alone is achievable. On a $3M ARR business, collecting 20 days faster frees $165,000 in working capital. That is an immediate value that requires no additional revenue, no new customers, and no product changes.

Payment Terms Comparison: Cash Flow Impact

| Payment Structure | Cash Flow Timing | Working Capital Benefit | Recommended For |

| Annual Prepay (10–15% discount) | Immediate upfront | Maximum — full year secured | All customer tiers |

| Net-15 (standard invoice) | 15-day cycle | Strong vs. net-30 default | SMB and mid-market |

| Net-30 (enterprise standard) | 30-day cycle | Baseline acceptable | Enterprise where required |

| Quarterly installments | 90-day cycle | Negative — avoid | Never if possible |

| Net-60 | 60-day cycle | Significant cash drain | Avoid — renegotiate |

When to Be Aggressive About Collections

Many SaaS companies are too passive about collections because they fear damaging customer relationships. This is a mistake. Customers who consistently pay late are learning that late payment carries no consequences, and they will continue doing it.

- Be aggressive when invoices hit 30 days overdue — polite reminders stop at that point and firm demands begin: payment is required within 48 hours

- Be aggressive with customers who pay late repeatedly — serial late payers need consequences, move them to prepay-only terms

- Push back when customers dispute invoices without legitimate cause — some customers dispute charges as a delay tactic, respond firmly with the signed agreement

- Stop spending time on small, chronically late accounts — a $200 per month customer is not worth hours of manual follow-up, automate them to prepay-only or let them churn

- Follow through on service suspension threats — companies with the strongest collection rates are willing to actually suspend access for non-payment, not just threaten it

Measuring Collections Performance

Track these metrics monthly alongside revenue and burn rate. The collection’s health affects cash runway just as directly as either of those numbers.

Days Sales Outstanding should be under 30 for most SaaS businesses. If it is rising month over month, investigate the cause immediately and do not wait for it to stabilize on its own.

The percentage of accounts receivable over 60 days should stay under 5%. Anything higher indicates systematic collection problems that will compound over time.

Monthly cash collections as a percentage of monthly revenue should be 90 to 100%. If $100,000 in revenue is being recognized while only $75,000 is being collected in cash, accounts receivable are building at a rate that may not be sustainable.

Failed payment recovery rate measures the percentage of failed credit card charges that are ultimately collected. Target 50 to 70%. Anything below 40% suggests the dunning process is either missing or ineffective.

Bad debt write-offs as a percentage of annual revenue should stay under 1%. Anything higher suggests the business is selling to customers who cannot actually pay, which is a customer qualification problem, not just a collections problem.

Review these numbers in every monthly management meeting alongside revenue metrics. A business with strong revenue growth and deteriorating collections metrics is building toward a cash crisis, and the metrics will show it before the bank account does.

Building a Collections Culture

The companies with the best collections do not treat accounts receivable as an accounting afterthought. They treat it as a strategic function with visibility, accountability, and clear consequences.

Make collection KPIs visible to the whole team. Post current DSO, aging buckets, and bad debt percentage, so that everyone can see them. When the numbers are visible, people care about them.

Hold account managers accountable for customer payment, not just for signed contracts. Credit a deal when cash is collected, not when the contract is signed. This single incentive alignment change produces faster collections without any process change at all.

Give the AR team authority to suspend service for delinquent accounts without escalating every case to leadership. Set clear policies, for example, accounts 45 or more days overdue are suspended, and let the team execute. Requiring CEO approval for every suspension creates delays that signal to customers that enforcement is not real.

Review problem accounts every week. Do not let invoices age to 60 or 90 days before anyone looks at them directly. Weekly AR review meetings covering every invoice over 45 days old, catch problems while they are still solvable.

Celebrate collections wins the same way wins in sales get celebrated. When the AR team collects a $50,000 invoice that was 90 days overdue, recognize it publicly. The revenue value of that collection is identical to a new sale of the same size, and it required no customer acquisition cost.

The Cash Collections Impact on Runway

Here is the math that makes this critical for every SaaS business.

A $2M ARR company burning $150,000 monthly has a runway determined by cash in the bank, not by the revenue figure on the income statement.

In scenario A, DSO is 45 days, and the accounts receivable balance is $250,000. Cash in the bank is $900,000. Runway is 6 months.

In scenario B, after improving collections, DSO drops to 20 days, and the accounts receivable balance falls to $110,000. Cash in the bank rises to $1,040,000 because the $140,000 previously trapped in receivables has been collected. Runway is now 6.9 months.

Same revenue. Same burn rate. Better collections added nearly a month of runway. In a fundraising environment where another month can be the difference between closing a round and not closing one, this is not a minor operational detail. It is a strategic priority.

FAQ

Q: Should we offer early payment discounts to improve collections?

Maybe. Calculate the cost first. A 2% discount for net-10 instead of net-30 costs you 2% of revenue but cuts DSO by 20 days. On a $2M ARR business, that’s $40K in lost revenue annually but $110K in working capital freed up. If you’re cash-constrained, that tradeoff makes sense. If you’ve got 18 months runway and strong cash position, keep the revenue and accept slower collections. Test it with large customers first before applying broadly.

Q: How do we handle customers who consistently pay late without damaging the relationship?

Set clear expectations and enforce consequences consistently. Tell the customer “Your account is being moved to prepay terms due to payment history. You’ll need to pay in advance each month going forward.” This isn’t punishment, it’s risk management. Most customers will accept it. The ones who won’t accept it probably aren’t customers worth keeping—they’re financing their business with your cash. Good customers understand that prompt payment is part of the relationship.

Q: What’s the best way to reduce failed payment churn in card-based billing?

Three steps: First, implement proper dunning with 3-5 retry attempts over 14 days. Second, make it extremely easy to update payment information with clear emails and one-click update links. Third, use account updater services (offered by Stripe and most processors) that automatically update expired cards with new information from card networks. This recovers 60-70% of failed payments that would otherwise churn. For high-value customers, add human outreach before cancellation—have customer success call them personally when payment fails.